21 May 2026

Equity research Angler Gaming, Q1 2026: Growth and margin expansion signals inflection point

21 May 2026

Read the full research update here:

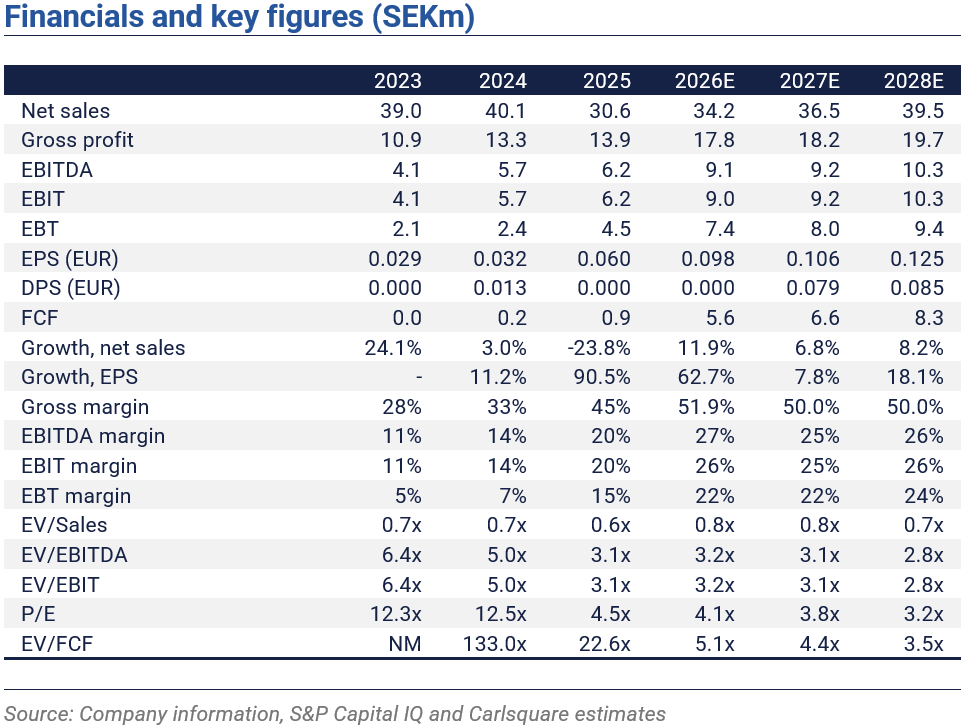

Angler Gaming delivered a strong quarter with a return to revenue growth trajectory, in line with our estimate, and an EBIT beat by a full 49%. The gross margin expanded sharply to 58% from 43% in Q1 2025. The trading update shows average daily NGR running 24.84% above the full Q2 2025 level, signalling clear momentum.

Gross margin expands as the B2B transition delivers

Net revenue rose in Q1 2026 by 1.6% to EUR 8.3m, in line with our EUR 8.2m estimate. Growth was driven by the B2B business as the revenue contribution from B2C remains limited at 3.5% of Group revenue. The growth returned to positive trajectory after six quarters of negative comparables driven by the renegotiated B2B model effective January 2025.

In addition to returning growth, the most significant development is the sharp margin expansion, confirming that the renegotiated B2B model is delivering as intended. Gross profit rose 38% to EUR 4.8m, with a gross margin of 58%, up from 43% in Q1 2025. This is a direct consequence of payment-related costs now being borne by B2B partners. Our gross profit estimate was EUR 3.6m. With a marginal increase in OPEX, EBIT grew 68% YoY to EUR 2.9m, resulting in a 35% margin and demonstrating operational leverage. Our EBIT estimate was EUR 1.9m. Cash flow from operations was negative at EUR -0.1m due to working capital movements, leaving room for improvements.

Trading update points to accelerating growth in Q2

With the platform now fully configurable by B2B partners and affiliate subsidiary Marlin Media having launched marvnBoost, the Q2 trading update adds further encouragement. Average daily net gaming revenue (NGR) is running 24.8% above Q2 2025, a clear acceleration from the 7.5% growth indicated at Q4 2025. Should Q2 continue on the trajectory the trading update suggests, the operational leverage built into the revised B2B model means profit growth should again comfortably outpace revenue growth.

Estimates raised materially, fair value up to SEK 6.5

Our revenue estimates are broadly unchanged, on average up by ~1% during 2026-28E. However, the strong quarter warrants a material upward revision to profitability. We view the margin improvement as structural rather than transitory and lift our gross profit forecasts for 2026-28E by an average of 13%, which, in the context of the Q1 report, could arguably be considered conservative. With continued growth and operational leverage feeding through, our EBIT estimates for the same period move up by an average of 20%.

Our new fair value is SEK 6.3 per share (5.1) over a 6-month investment horizon. At the current share price, the stock trades at an EV/EBIT NTM of 3.4x, a discount of ~63% to the reference group. We consider this discount excessive, given the demonstrated margin expansion and the outlook for a more sustainable growth path.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Similar News