27 May 2026

Equity research, Lokotech H2 2025: Orders stack up and warrants sweeten the case

8 Apr 2026

Read the full report here:

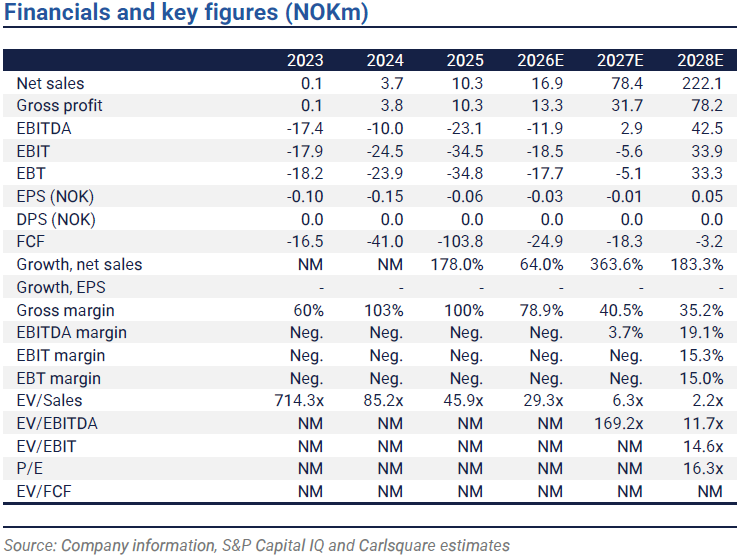

In 2025, Lokotech reported revenues of NOK 10.3m, below our estimate from March 2025 due to the delayed launch of Hashblade. The company now expects first deliveries to be shipped in H2 2026. We see an attractive opportunity in subscribing for the warrants with a strike price of NOK ~0.61.

Strong operational momentum for Powerpool

For FY 2025, net sales came in at NOK 10.3m, well below our forecast of NOK 36m from March 2025. The gap reflects a delayed launch and sales of Hashblade. Revenues were instead driven by Powerpool, which is showing clear operational momentum, with rising hashrate and a growing base of connected customers. That said, this did not translate into sequential growth in H2 2025 as prices for cryptocurrencies retraced while the company to a greater extent used affiliates during the ramp-up phase, which in turn held back the company’s average fee level.

For the full year, EBITDA came in at NOK -23.1m versus our initial forecast of NOK -12m. The miss was driven by lower revenues and slightly higher OPEX. CAPEX of NOK -77.1m primarily relates to a prepayment for the mask set for the Scrypt ASIC chip, which is the core of Hashblade. At year-end 2025, cash stood at NOK 37.0m.

High interest ahead of launch evidenced by pre-orders

During 2025, the company completed extensive testing and tape-out preparations for its IC design. On 15 December 2025, the final chip design run was initiated ahead of handover to the foundry for manufacturing. The company now expects first deliveries to take place in H2 2026. According to the report, the value of existing Hashblade pre-orders is in the range of USD 7–13m. Cancellations were limited to USD 53,000, despite a price correction in Scrypt-based coins. One possible explanation is that Hashblade’s superior energy efficiency becomes relatively more valuable in a low-price environment, and that long-term players have limited economic incentive to cancel. In addition, US authorities’ classification of LTC and DOGE as digital commodities, via the SEC and CFTC, could further support demand.

Clear potential upside versus the warrants’ strike price

We forecast FY 2026E net sales of NOK ~17m, with just under one third from Hashblade sales, where first deliveries take place in H2. Given leading energy efficiency and potential in, among other areas, a number of AI applications, we assume a sharp ramp in hardware sales in the coming years. In our scenario, the business reaches EBITDA break-even in 2027E and, with strong growth and a scalable model, we see the EBITDA margin trending towards ~19% in 2028E.

In our base case, we estimate fair value at NOK 1.1 per share, which makes the outstanding warrants, with a strike price of NOK ~0.61 per newly subscribed share, attractive.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Similar News