Senior Equity Analyst

Equity research CDON: Preview Q1 2026 – Continued growth, but initiatives will likely hamper earnings

13 Avr 2026

We expect continued growth, albeit slightly below the strong Q4 level. Focus is on implementing growth initiatives and on the outlook in light of recent developments, including the onboarding of major merchants and changes to the marketing channels.

Continued growth expected despite slight channel issues

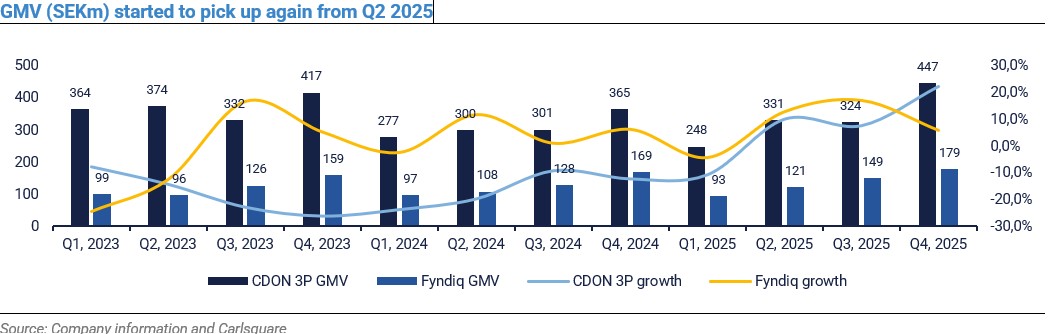

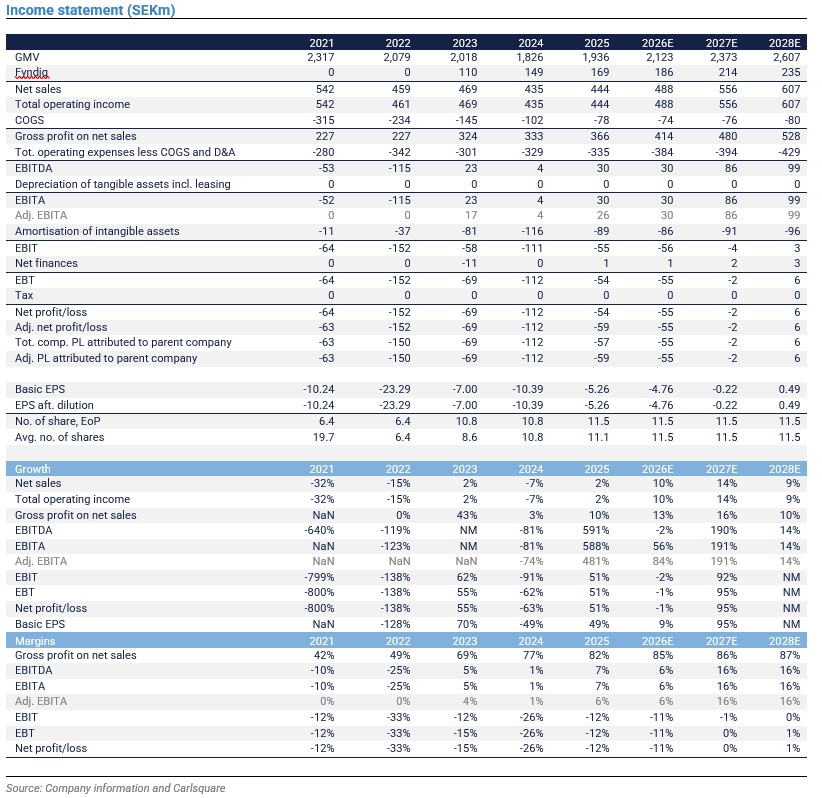

We expect continued GMV growth in line with recent trends; however, seasonality is naturally weaker in Q1 than in Q4. We estimate that traffic has developed slightly below our previous assumptions. Still, we assume 6% GMV growth, below the 15% growth rate in Q4 2025.

One factor behind the possible (slight) shortfall is likely that CDON removed its products from the price comparison site Prisjakt in February as increased fees made the collaboration uneconomical. We estimate that Prisjakt accounted for about 5% of traffic to CDON.se until the termination. We believe the impact on overall traffic so far has been limited, suggesting that decent growth in other channels has mitigated the effect. Given the public backlash against Prisjakt’s pricing policy from several e-commerce players, we believe the bottom-line impact is negligible. We estimate that most of the traffic to CDON group sites comes from other sources, primarily organic search. The onboarding of new major European merchants could help underpin growth from Q1 onwards.

According to Svensk Handel’s e-handelsindikatorn survey, e-commerce in Sweden increased by 1% and 15% in January and February 2026, respectively. Typically, this survey is quite volatile and somewhat difficult to interpret. However, it supports the view of continued e-commerce growth following the good development in 2025.

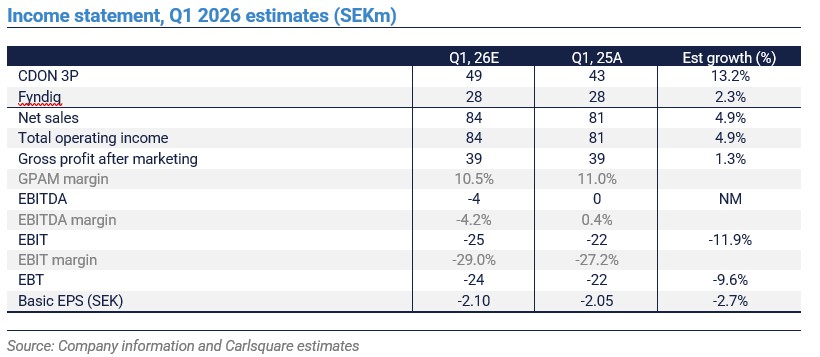

Given our assumptions about traffic mix, average order value, and take rate, this translates into net sales of SEK 84m (81). We assume costs for growth initiatives, such as the onboarding of tech resources, have resulted in an OPEX increase, resulting in an EBITDA loss of SEK -4m (0). The earnings estimates are uncertain at this point, as CDON has not communicated the exact cost and timing of its growth initiatives.

Disclaimer

Carlsquare AB, www.carlsquare.se, hereinafter referred to as Carlsquare, is engaged in corporate finance and equity research, publishing information on companies and including analyses. The information has been compiled from sources that Carlsquare deems reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be considered a recommendation or solicitation to invest in any financial instrument, option, or the like. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for either direct or indirect damages caused by decisions made on the basis of information contained in this analysis. Investments in financial instruments offer the potential for appreciation and gains. All such investments are also subject to risks. The risks vary between different types of financial instruments and combinations thereof. Past performance should not be taken as an indication of future returns.

The analysis is not directed at U.S. Persons (as that term is defined in Regulation S under the United States Securities Act and interpreted in the United States Investment Companies Act of 1940), nor may it be disseminated to such persons. The analysis is not directed at natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign laws or regulations.

The analysis is a so-called Assignment Analysis for which the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published on an ongoing basis during the contract period and for the usually fixed fee.

Carlsquare may or may not have a financial interest with respect to the subject matter of this analysis. Carlsquare values the assurance of objectivity and independence and has established procedures for managing conflicts of interest for this purpose.

The analysts Niklas Elmhammer and Markus Augustsson do not own and may not own shares in the analysed company.