Equity research Enrad, Q4 2025: A Sweden push to accelerate growth

1 Mar 2026

Read the full report here:

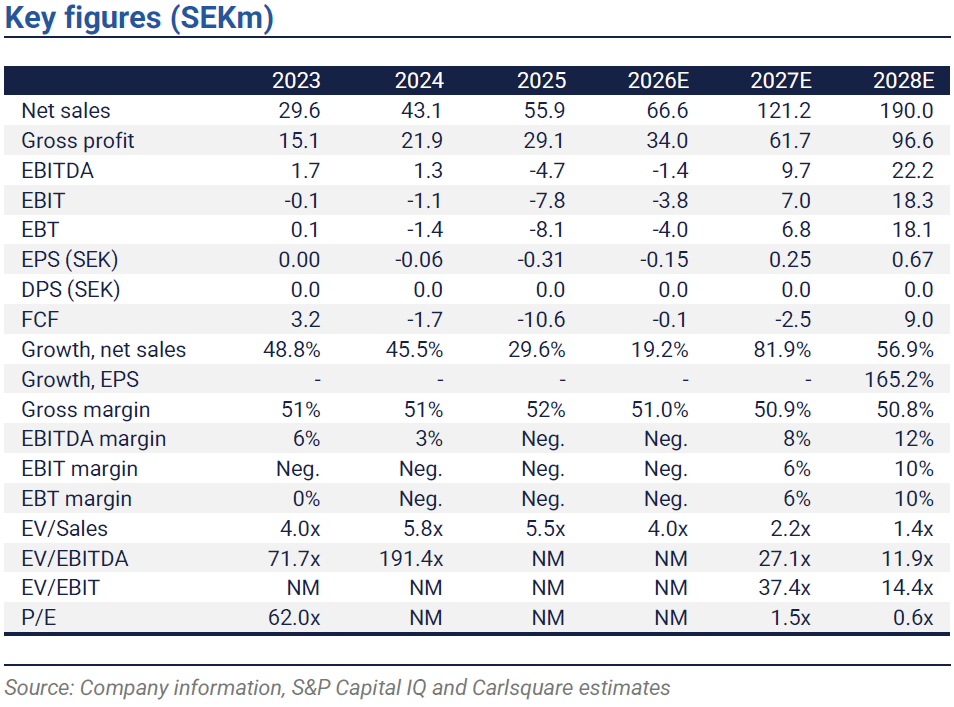

Enrad’s FY2025 net sales of MSEK 55.9 grew 29.6% YoY but fell approximately 7% short of our estimate. A sluggish market is not stopping Enrad. Instead, the company has appointed a sales manager and another salesperson to intensify the sales activities in Sweden. We expect this initiative to start impacting sales in H2 2026.

A soft close to 2025 on a sluggish market

FY2025 net sales of SEK 55.9m grew 29.6% YoY but missed our SEK 59.9m estimate by roughly 7%. Gross margin of 52.1% printed 2.2 p.p. above our 49.9% forecast. Despite the margin beat, EBIT of SEK -7.8m came in weaker than our SEK -5.3m estimate, driven by the Q4 2025 revenue shortfall. Full-year EPS landed at SEK -0.31 versus our SEK -0.02 estimate. The cash position at year-end stood at SEK 19.6m. With continued ability to borrow against customer invoices and inventory, the board’s assessment is that no capital raise is likely to be required in 2026.

Increased sales activities in Sweden

The lion’s share of growth came from Sweden, despite limited domestic sales efforts. The home market has clearly been underexplored. Appointing a dedicated Sales Manager for Sweden should strengthen the pipeline, deepen customer relationships, and support the onboarding of an additional salesperson joining in March. The move signals a clear intent to fully unlock the domestic opportunity. We expect the increased sales activity to start feeding through in H2 2026, while the push into the Netherlands and Belgium may yield a somewhat delayed effect relative to our previous assumptions.

Regarding production capacity and operational leverage, Enrad can already manufacture north of SEK 80m from the existing facility. The relocation to a new production site (first flagged in the Q4 2024 report) lifts capacity to above SEK 100m with no incremental headcount. Management noted in the Q4 report that most capex ahead of the move is already in place, suggesting the transition is near-term. This is a capital-efficient setup: incremental revenue up to SEK 100m should flow through with limited additional OPEX pressure, providing meaningful operating leverage as volumes ramp.

Revised valuation

We have cut our net sales estimates for 2026–28E by ~17% on average, reflecting sluggish market conditions and limited visibility on when demand will meaningfully take off, leading to lower profitability in the mid-term. Despite the estimate cuts, we raise our fair value to SEK 11.5 (9.0). The revision is driven by a shift in valuation approach: We now place greater weight on the DCF to better capture long-term potential, which more than offsets the lower topline and profitability assumptions. Our fair value implies EV/Sales 2027E of 2.4x and EV/EBIT 2028E of 16.2x. The peer group currently trades at a median EV/Sales NTM of 2.3x and EV/EBIT NTM of 18.7x.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.