Head of Financial Sponsor Coverage

Carlsquare Private Equity Insights: Q1 2026

24 Avr 2026

After an exceptionally strong H2 2025, including a record-breaking Q3 for DACH PE Exits, Q1 2026 has opened cautiously. Yet despite the subdued start, significant structural forces create strong tailwinds for PE deal activity, and the conditions for a meaningful acceleration in the second half of 2026 are increasingly in place.

Executive Summary:

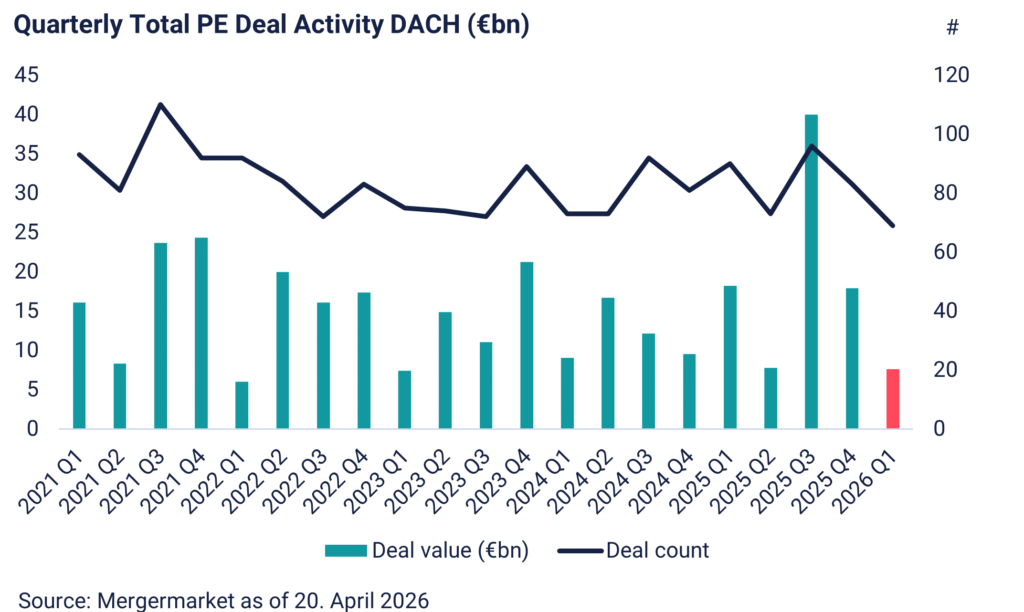

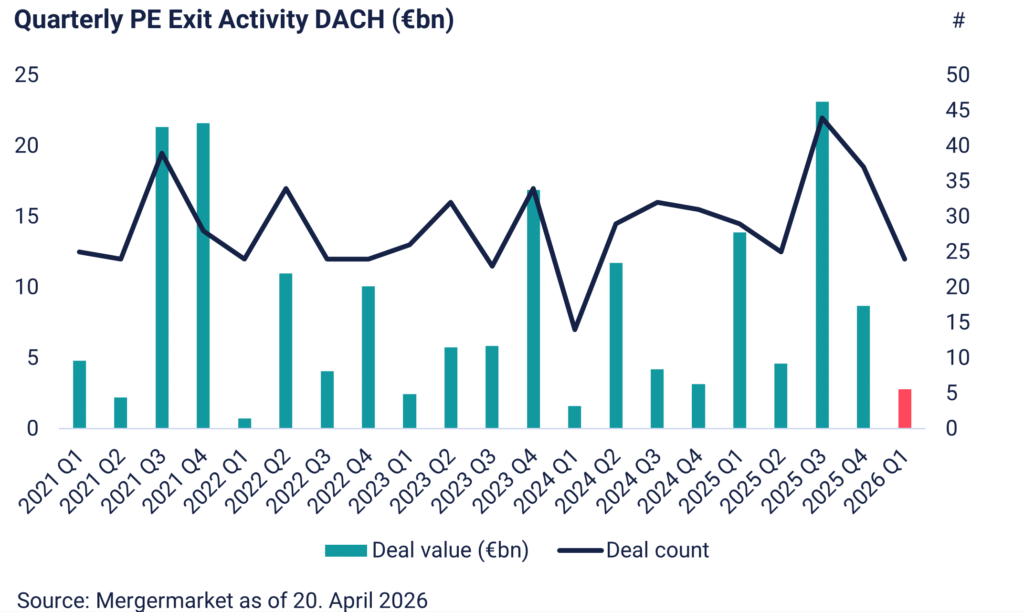

- Q3 2025 saw a strong performance for DACH private equity deal activity and a record number of exits, marking the high point of a volatile but resilient year for the market.

- Q1 2026 has started quietly. Compared to Q1 2025, the PE transaction count dropped by 23.3% and the number of exits by 17.2%. However, accelerating pitch activity and persistent structural tailwinds, such as large amounts of dry powder, elevated holding periods, and LP pressure for distributions, point to a materially stronger second half of the year.

- The Iran vs. USA conflict ignites global markets, higher financing costs are anticipated.

- Our last PE survey identified Industrial Technology as the most requested sector for insights and deal flow (21%), ahead of Business Services (19%) and Healthcare (17%). This makes Industrial Technology the natural choice for the Sector in the Spotlight of this edition.

- Finally, in our inaugural Partner Interview, we sat down with Martin Preuss, Partner and Head of DACH at Inflexion, to discuss the key drivers behind their successful fundraising, how Inflexion is navigating current market conditions, and his predictions for the DACH PE Market 2026. Read the full conversation here.

1. Private Equity Market Update: DACH

2025 Review:

The year began with significant volatility before culminating in an exceptionally strong second half for DACH Private Equity. At roughly €40bn in PE deal value and the highest transaction count since 2021, Q3 2025 stood out as a landmark quarter. DACH Exit activity followed suit as sponsor-backed exits in Q3 reached approximately €23bn, and the number of exits reached record levels. Q4 2025 saw a natural pullback from those highs, consistent with the digestion of a large transaction wave.

Three key factors drove the surge in Q3 DACH PE deal activity:

- Sponsors had delayed exits for several years and a number of deals had been placed on hold due to tariff uncertainty. A large portion of this long-accumulated backlog of transactions finally cleared in Q3 2025.

- Stabilizing interest rates improved financing conditions.

- Easing tariff uncertainty reduced the risk premium on deal execution.

Q1 2026:

Several key drivers generate significant momentum for deal activity going into 2026:

- Dry powder across DACH PE funds remains at historically elevated levels, having surpassed €30bn since the end of 2025.

- Holding periods have stretched well beyond historical averages. Notably, 26% of DACH PE assets haven’t changed hands in 7+ years.

- As a result, LP pressure for distributions is intensifying.

Taken together, these dynamics create strong tailwinds for PE deal activity in 2026, with the transaction market increasingly supply-driven rather than demand-constrained.

So far, 2026 has opened cautiously, as the Q1 data confirms. Deal values and counts remain low, reflecting the typical slow start to a new year and the natural digestion period following an active second half of 2025. Compared to Q1 2025, the total PE transaction count in Q1 2026 dropped by 23.3% and the number of exits by 17.2%.

However, in our view several factors point to a meaningful acceleration in deal flow. Even though elevated energy costs and AI-driven valuation uncertainty remain prevalent, Carlsquare is seeing a significant increase in pitch activity across sectors, pointing to a strong pipeline building beneath the surface. The fundamental drivers (dry powder, holding period pressure, and LP demand for liquidity) have not dissipated. Our expectation is that deal momentum will build up gradually through Q2 and into the second half, setting up 2026 as a stronger year than its quiet opening suggests.

Sources: Mergermarket (as of April 20, 2026); Pitchbook (as of December 19, 2025); Gain “The State of European Private Equity Report” (2026); Carlsquare Research

2. Sector in the Spotlight: Industrial Technology

In our Sector in the Spotlight, Steffen Leckert, Managing Partner and Head of Industrial Technology at Carlsquare, shares his views on the key dynamics shaping Industrial Technology M&A in the DACH region.

How would you summarize Q1 2026 for Industrial Technology M&A? What were the key factors shaping this environment?

M&A activity in the Industrial Technology sector remained relatively subdued in Q1 2026, continuing the muted momentum observed throughout 2024 and early 2025. Across the DACH region, announced transactions declined by 18%, totaling 112 deals compared with 137 in Q1 2025.

Several factors shaped this environment:

- Geopolitical tensions, particularly the Iran conflict and ongoing instability in the Middle East, have reignited concerns around global supply chains, delivery reliability, and energy price volatility

- Industrial companies with high raw material or energy exposure continued to face significant uncertainty regarding cost predictability and pricing power

- Despite this, sell-side preparation activity is clearly accelerating — a considerable pipeline of industrial assets is being readied for market, with launch timings sensitive to inflation trends, interest rate expectations, and energy market stabilization. Most owners remain prepared but will choose windows with visible improvement in sentiment

Overall, 2026 has started cautiously — yet with rising indications of pent-up supply coming to market as soon as macro conditions stabilise.

Which sub-sectors within Industrial Technology are you seeing the strongest investor appetite for?

Investor appetite is strongest in segments with structural growth drivers and limited global volatility exposure:

- Defense & Security Technology: Europe’s multi-year rearmament cycle, driven by NATO commitments and national modernization programs, is fueling demand for sensors, communication systems, unmanned platforms, and electronic warfare solutions

- Industrial Services: Building technology services (HVAC, electrical installation, smart building retrofits) and infrastructure services (maintenance, inspection, engineering services for utilities and transportation assets) offer recurring revenues and local exposure — highly attractive for financial sponsors

- Data Center Supply Chain: Suppliers of cooling, power management, connectivity, security systems, and automation benefit from high-visibility AI-driven capex programs across hyperscale and edge data centers in Europe and the US

- Energy Transition & Electrification: Grid modernization, EV charging, power electronics, battery thermal management, and hydrogen-ready infrastructures continue to attract considerable sponsor attention

Deal processes in these sub-sectors are competitive, often attracting both mid-market funds and large-cap infrastructure investors.

How have deal processes and valuation multiples in Industrial Technology evolved in the current environment?

The valuation environment has been resilient in early 2026:

- The S&P 500 Industrials Index reached an all-time high of 1,512 on 2 March 2026 before correcting 7–8% following the Iran escalation — still above long-term average levels

- AI is creating productivity benefits (predictive maintenance, automation, process optimisation) rather than displacement, supporting stable to rising valuations in key verticals. Sponsor interest is particularly high where structural demand is robust

Across the broader Industrial Technology sector, most sub segments currently trade close to their 5 year median multiples, with premium valuations concentrated in areas benefitting from the above outlined factors.

The following selected verticals feature particularly high valuation multiples (EV/NTM EBITDA) compared to their respective historic averages:

| Vertical | EV/NTM EBITDA |

| Robotics (incl. Humanoid & Unmanned Vehicles) | >20x |

| Flow & Process Control | >15x |

| Safety & Building Technology | >13x |

| B2B Electronics & Connectivity | >10x |

| Industrial Services (Engineering, HVAC, Environmental) | >10x |

Which factors will be most decisive in shaping financial sponsor activity in Industrial Technology in the second half of 2026?

We expect a notable increase in sponsor activity in H2 2026, driven by:

- Embedded technology resilience: Hardware/software integration makes Industrial Technology less vulnerable to rapid technological substitution than Software, Digital Commerce, or Consumer Tech

- Strong investment cycles: Defense, robotics, energy transition, and data center infrastructure offer multi-year, high-visibility capex programs that support investment theses even amid macro uncertainty

- A maturing PE backlog: Many sponsors hold Industrial Technology assets acquired in 2019–2021, primed for divestment after an extended hold period given the subdued exit environment of 2023–2025

- Improving macro clarity: Any easing of energy price volatility, trade friction, or supply chain disruptions would materially improve forecastability and accelerate delayed sale processes

- Relative sector attractiveness: With Software facing AI-driven pricing pressure and Consumer sectors showing inconsistent demand patterns, investors are increasingly returning to industrial businesses with tangible technologies, local moats, and stable cashflows

Carlsquare View: If macro conditions stabilise, H2 2026 could represent the strongest M&A window for Industrial Technology since 2021 — driven by pent-up sell-side supply and renewed buy-side conviction.

Our two most recent Carlsquare Industrial Technology deals:

Carlsquare advised Lacon Group on its acquisition by Incap

Carlsquare advises Afinum Management on €75m sale of Kappa optronics to Theon International Plc

Source(s): Mergermarket (as of April 20, 2026); S&P Capital IQ (as of April 20, 2026); Carlsquare Research

3. Financing Market Update from Carlsquare Debt Advisory Team

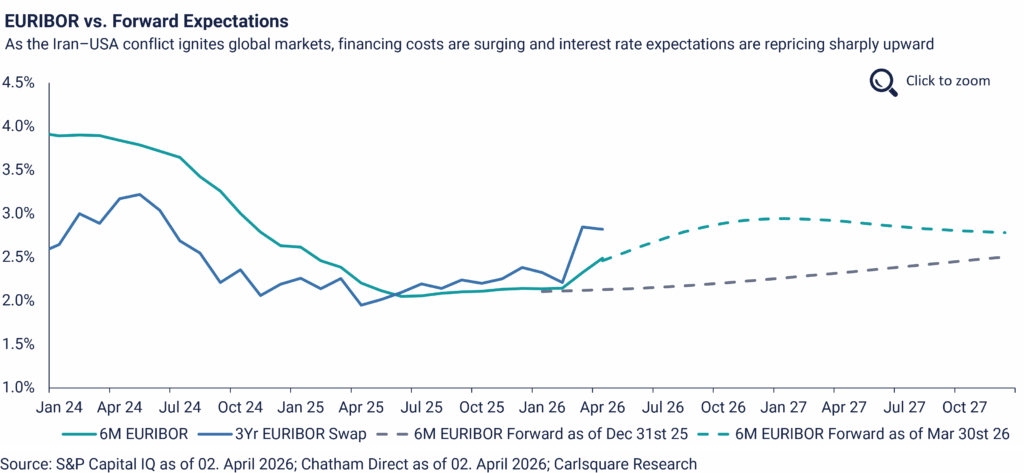

The ECB held rates unchanged at their latest meeting in March at 2.0% since June 2025 but warned equally that soaring energy prices due to ongoing war in Ukraine and newly outbreak of the Iran war would have a material impact on inflation. The ECB is expecting the inflation rate to be at 2.6% for this year compared to a previous estimate of 1.9% in December 2025. Likewise, the Bank of England decided in their most recent meeting to keep the interest rate steady at 3.75%. As illustrated in the Carlsquare Euribor vs. Forward Expectations chart, a comparison of forward curves at end-2025 and end-March 2026 reveals that markets have already priced in close to 80 bps of near-term risk with three interest rate hikes this year, reflecting a notable increase in uncertainty among market participants.

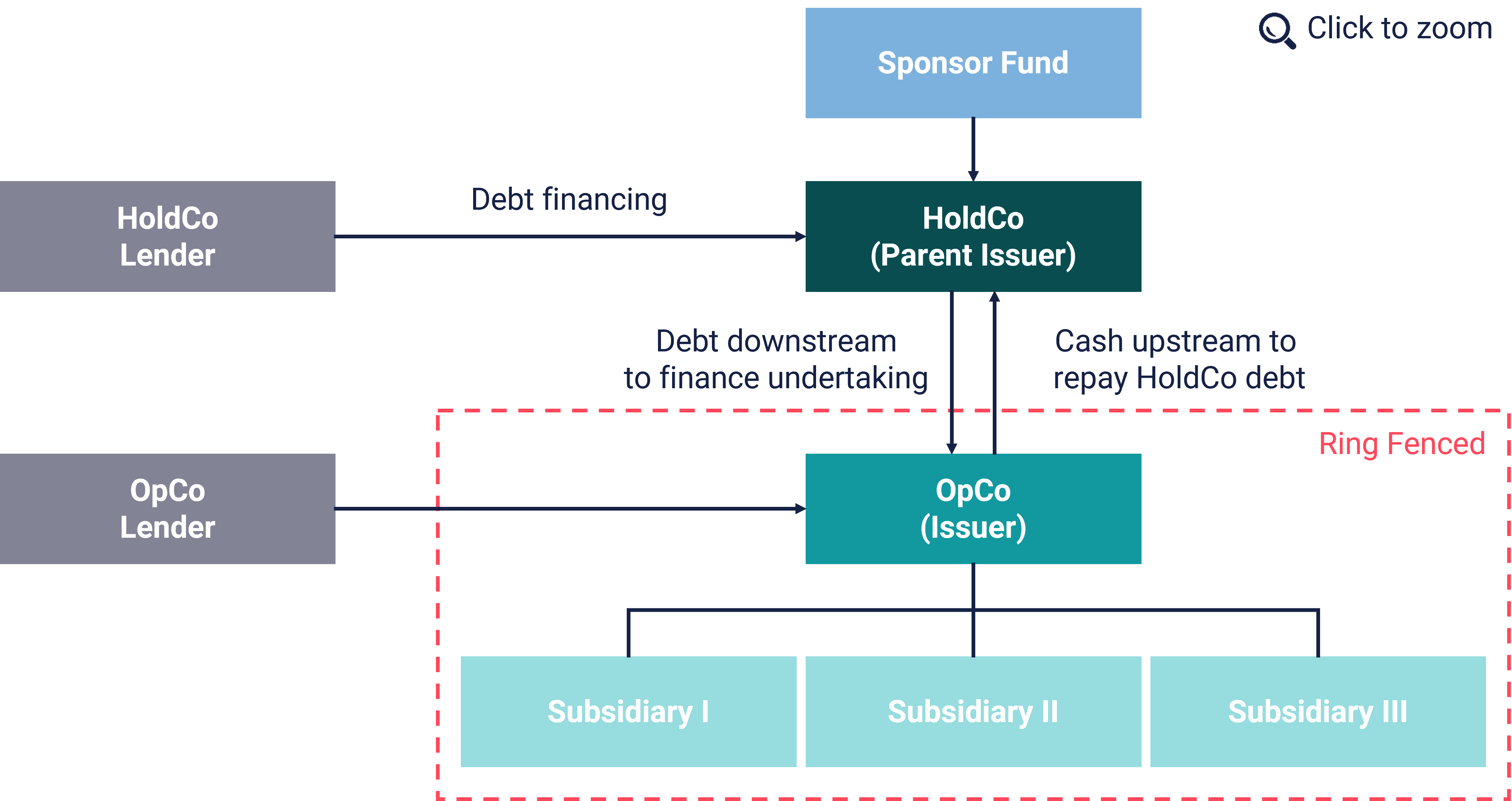

HoldCo Financing – An effective instrument for additional leverage

HoldCo Financing is an effective tool for additional leverage while preserving cash at OpCo level: It avoids immediate cash interest burden at the operating company – relevant when free cash flow is tight or reinvestment needs are high.

- Closing valuation gaps: Junior/non-cash-pay tranches can help buyers reach higher valuations while keeping deal economics workable.

- Mid-hold liquidity bridge: With longer holding periods, PIK can bridge capital needs for growth or liquidity management.

- Add-ons without reopening senior terms: HoldCo PIK can fund bolt-on acquisitions without renegotiating the senior debt package.

- Dividend recap / LP liquidity: Depending on structure, can create “top-of-structure” liquidity without increasing OpCo cash interest.

4. Carlsquare PE Conversations: Martin Preuss, Partner and Head of DACH at Inflexion

Inflexion Private Equity is one of Europe’s most active mid-market buyout firms. We sat down with Martin Preuss, Partner and Head of DACH at Inflexion, to discuss their newly raised €4.5bn Buyout Fund VII, their DACH ambitions, and how they are navigating an M&A environment shaped by AI and geopolitical uncertainty.

Recent Carlsquare Private Equity Deals

For any questions feel free to reach out to our authors Armin Sieber, Head of Financial Sponsor Coverage or Steffen Leckert, Managing Partner & Head of Industrial Technology.

Managing Partner and Head of Debt Advisory

Similar Insights