Managing Partner

Software is back: the rally is spreading from AI hype to Microsoft, Oracle and ServiceNow

3 Juin 2026

Share prices of U.S. software companies have picked up sharply in recent days. At the top of the list we unsurprisingly find hyped AI names and cybersecurity companies. But what’s most interesting is that the move also appears to include the larger, more stable players – such as Microsoft, Oracle and ServiceNow.

If this move holds, we may be seeing early signs of stabilisation in software valuations – after the valuation pressure that has characterised the sector in recent years.

Over the past few months, market attention has largely been on chipmakers and other companies clearly associated with AI. At the same time, the narrative has been that the AI revolution could put pressure on software companies’ revenues (for example through pricing pressure and faster competition). That has contributed to capital rotating from software toward hardware – the “picks and shovels” of the AI value chain.

There are no clear signs of a trend shift away from chipmakers. But investors now seem increasingly willing to buy broadly into one of the most beaten-up parts of the equity market: software.

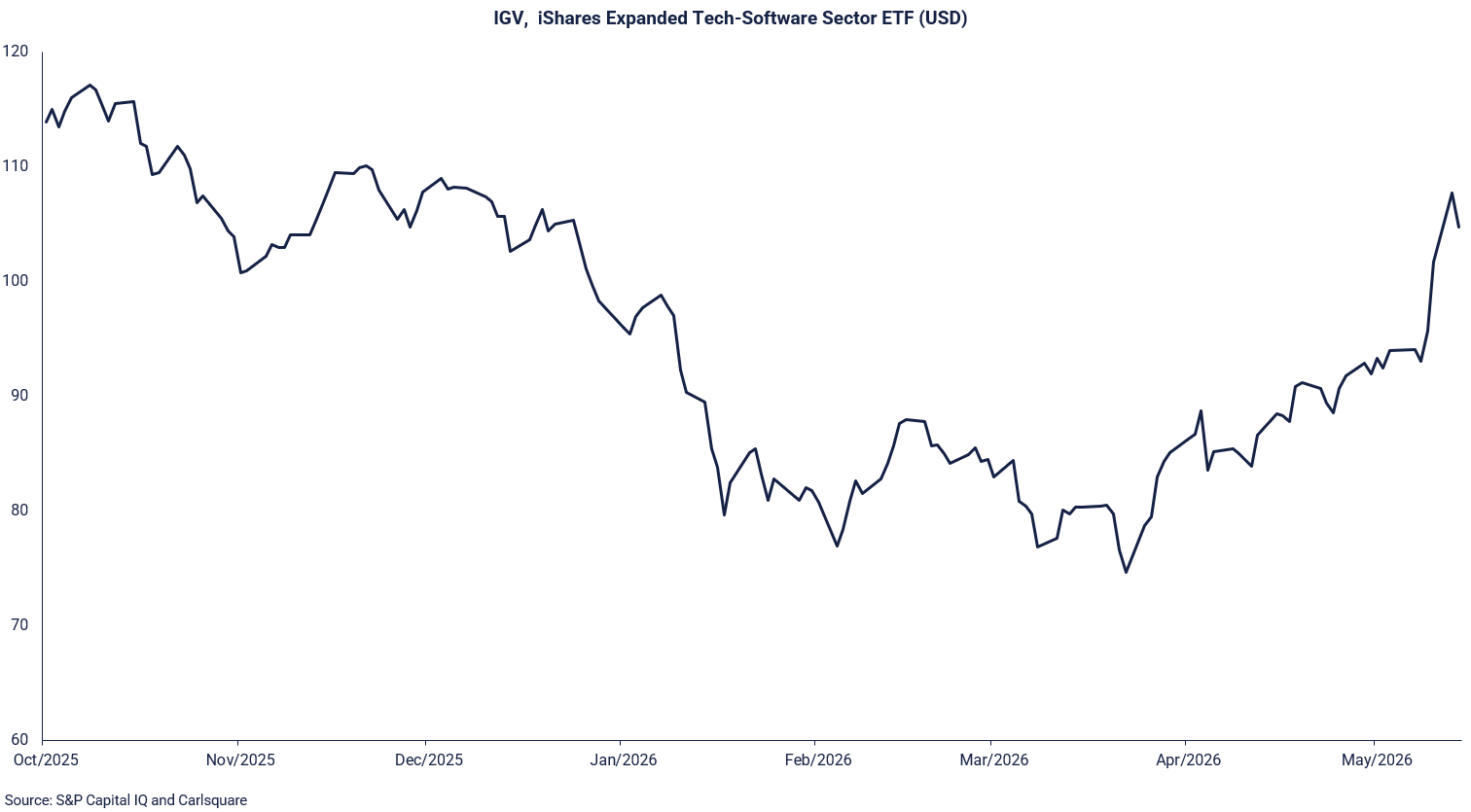

Over the past two months, the IGV ETF – which holds just over 100 U.S. software companies – has risen sharply, up 45%. As always, dispersion between individual stocks is large. At the very top are names like BlackBerry, up nearly 200%. But what stands out is that large, mature companies have also moved meaningfully: Oracle is up around 67%, ServiceNow around 25%, and Microsoft around 18% over the same period.

This matters for the private market as well. In private M&A, we have seen multiples fall from around 10x sales to, in many cases, 3–4x sales. The result has been a market that is partly frozen. Many entrepreneurs quite reasonably ask: why sell at such low multiples? Markets have a tendency to overshoot – both ways.

If the re-rating in listed software – especially among the larger U.S. quality names – continues, and if seller expectations in the private market adjust somewhat at the same time, the gap between buyers and sellers may start to close.

In that scenario, our view is that the transaction market could begin to move in earnest again.

What has driven the rally?

If we look at IGV (iShares Expanded Tech-Software Sector ETF) – a broad, index-like basket of just over 100 U.S. software companies – a few clear patterns emerge over the past two months:

Cybersecurity has been one of the strongest categories.

For example, CrowdStrike, Palo Alto Networks and Fortinet have performed very strongly. The explanation is often that cybersecurity is viewed as “must-have” in IT budgets even when other projects are postponed – and that AI increases both the attack surface and the willingness to invest in protection.

DevOps/observability and IT operations have regained momentum.

Names like Datadog stand out. In this group, the market tends to reward companies that sit close to cloud trends and productivity/automation, with clear scalability in the business model.

High-beta and “theme” exposure has produced extreme moves.

A handful of very volatile stocks have posted exceptional gains (e.g., BlackBerry). It’s a reminder that parts of the rally can be driven by sentiment, flows and positioning – not just fundamentals.

The key shift: mega-cap software is moving higher too.

Oracle (+67%), ServiceNow (+25%) and Microsoft (+18%) suggest this is not only a small/mid-cap rally. When the larger quality names reprice, it can reset the valuation anchor for the broader sector.

If you’re an owner, PE investor, or management team in software and want to discuss what this shift could mean for valuations and deal timing – feel free to contact us.