Senior Equity Analyst

Equity research Candles Scandinavia, Q1 2026: A scent of synergies

8 Mai 2026

Read the full report here:

The beginning of the year was slower than we had assumed. However, a key message is that the integration work with HashtagYou is running according to plan. We expect quarterly reports showcasing production synergies to be catalysts for the share price in H2 2026.

Slow season and difficult comparison hamper sales growth in Q1

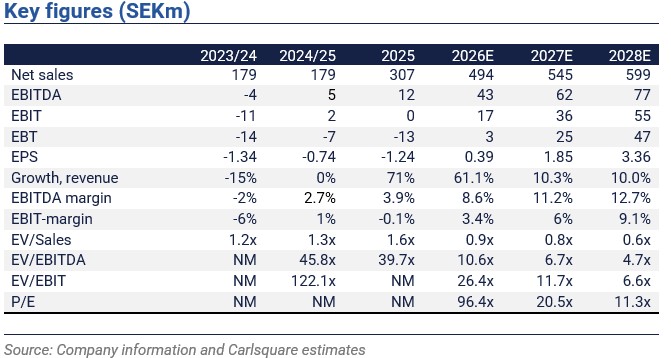

Candles Scandinavia’s net sales were again boosted by the acquisition of HashtagYou, increasing 98 per cent to SEK 82m (42). The impact from the acquisition was 110 per cent; consequently, the Private Label segment contracted by 12 per cent. Drivers behind the decline are strong comparables and FX headwinds. Hence, the string of growth quarters running from Q2 2024/2025 was broken. In sum, sales were lower than our forecast; however, seasonality is arguably more pronounced in the new structure and following the shift to calendar year reporting. Although comparable financials were not published, Candles says HashtagYou’s revenue increased.

Preparations for production integration are proceeding according to plan

EBITDA declined to SEK -2.3m (0.9), burdened by lower volumes in the Private Label business. While OPEX-to-sales is elevated following the acquisition of HashtagYou, we conclude that costs were still somewhat lower than expected in the quarter. Overall, it is hard to draw firm conclusions from the lower profitability as volumes are seasonally weak. The production relocation of HashtagYou’s range to the company’s own factory in Örebro is the single most strategically important operational event right now. Management says the project is progressing to plan, with the launch of in-house manufactured products expected towards the end of Q2. The profitability impact is expected to start in H2 2026, with full run-rate effects from 2027. The CEO reiterates the outlook that “2026 has every chance of becoming the company’s best year to date, both in terms of profitability and cash flow”. The recently published annual report reveals that margins after raw materials and supply costs improved markedly in 2025, mainly due to the acquisition and the new group structure. This further supports the case for scalability, we believe.

Prospects for significant profitability improvement remain

Following the report, we expect lower sales growth from external Private Label customers in the medium term and accordingly reduce our net sales estimates by an average of 1.5% for 2026-2028E. As a result, we trim our corresponding EBITDA estimates by approx. -5 per cent. Also, cash flow from operations was on the weaker side at SEK -12.5m in the quarter (4.2) and the cash position was SEK 12.1m at the end of Q1 2026, vs SEK 17.6m at the end of December 2025. Due to somewhat lower estimates and increased net debt, we adjust the base-case valuation to SEK 50 (SEK 54) per share. We still argue that the case for solid growth combined with significant improvement in profitability in the medium term remains. This contrasts with the modest EV/sales 2026E multiple of 0.9x, compared to peers’ 1.3x.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.