Senior Equity Analyst

Equity research, Zinzino Q1 2026: First impression – Healthy margin trend continues

22 maj 2026

Zinzino published its Q1 2026 interim report today. Below is our initial analysis of the results, including deviations from our updated estimates

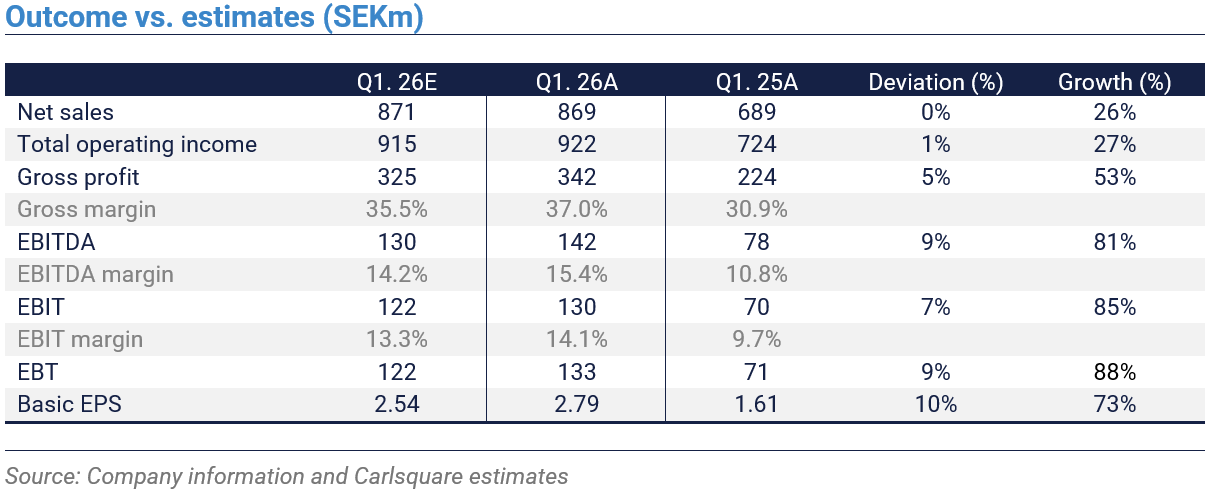

In line with the preliminary sales pre-announcement in April, Zinzino reported a 26 percent revenue growth in Q1 of 2026. The main regional drivers of absolute sales were again Central Europe and North America.

Margins were again clearly higher than our forecast and Zinzino’s financial targets. This was primarily due to a higher gross margin than we had assumed. Zinzino cites a weaker USD, a positive geographic mix, and normalised remuneration levels for distributors during the quarter as reasons for the improvement. In sum, the solid margin trend continues. The comments regarding the North American market are more optimistic than we had feared, however, the contribution from acquisitions seems lower than we had assumed.

The CEO, Dag Bergheim Pettersen, described the first quarter as a “record quarter” and expressed his satisfaction with achieving economies of scale while maintaining strong growth and successfully integrating new acquisitions. The strategic focus for 2026 includes profitable growth, pursuing further acquisitions, investing in the company’s digital platform, and maintaining cost control.

- Total revenues increased by 26% in Q1 2026 to SEK 922m, which aligns with the preliminary sales figures already disclosed in April.

- Gross profit grew by 53% to SEK 342m, compared to our forecast of SEK 325m. Year over year, the gross margin increased by 5.1 percentage points to 37%, a further increase compared to the strong previous quarter.

- The EBITDA result increased to SEK 142m (78), corresponding to a margin of 15.4%. Our estimate was SEK 130m, corresponding to a 14.2% margin. The deviation was due to the significantly improved gross margin. Cash flow from operations soared to SEK 121m (21).

We intend to provide a research update on Zinzino shortly. Read the latest research update here.

Disclaimer

Carlsquare AB. www.carlsquare.se. hereinafter referred to as Carlsquare. is engaged in corporate finance and equity research. publishing information on companies and including analyses. The information has been compiled from sources that Carlsquare deems reliable. However. Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be considered a recommendation or solicitation to invest in any financial instrument. option. or the like. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied. reproduced. or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for either direct or indirect damages caused by decisions made on the basis of information contained in this analysis. Investments in financial instruments offer the potential for appreciation and gains. All such investments are also subject to risks. The risks vary between different types of financial instruments and combinations thereof. Past performance should not be taken as an indication of future returns.

The analysis is not directed at U.S. Persons (as that term is defined in Regulation S under the United States Securities Act and interpreted in the United States Investment Companies Act of 1940). nor may it be disseminated to such persons. The analysis is not directed at natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign laws or regulations.

The analysis is a so-called Assignment Analysis for which the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published on an ongoing basis during the contract period and for the usually fixed fee.

Carlsquare may or may not have a financial interest with respect to the subject matter of this analysis. Carlsquare values the assurance of objectivity and independence and has established procedures for managing conflicts of interest for this purpose.

The analysts Markus Augustsson and Niklas Elmhammer do not own and may not own shares in the analysed company.