Managing Partner

Process of Selling a Business in 5 Steps

27 maj 2026

A structured overview of the M&A sell-side process — from valuation to completion. Insight drawn from over 600 transactions advised by Carlsquare.

A business sale is among the most consequential decisions a shareholder will make. The transaction involves not only the realisation of enterprise value, but also the continuity of the business and the interests of everyone connected to it. Executing this process without a structured approach carries significant risk — financial, reputational, and operational.

This article outlines the five steps of a professional M&A sell-side process. It reflects the transaction experience of Carlsquare across more than 600 mandates. Whether a sale is under active consideration or still at an exploratory stage, this guide provides a clear framework for what the process entails and where the critical value drivers lie.

We guide entrepreneurs through this process every day, both professionally and personally. That is why we know which questions truly matter, where the critical junctures lie, and which details make all the difference.

Key Points at a Glance

- A structured sell-side process comprises five steps: Valuation & Preparation, Information Memorandum, Buyer Outreach, Due Diligence, and Negotiation & Completion.

- The end-to-end transaction timeline typically ranges from 6 to 12 months.

- Adjusted EBITDA is the primary valuation metric and the basis on which enterprise value is negotiated.

- The Information Memorandum is the central transaction document. It presents the investment case to prospective acquirers in a structured and compelling format.

- A competitive process, with multiple acquirers submitting indicative offers simultaneously, is the most effective mechanism for maximising transaction value.

- Due diligence is the acquirer’s systematic risk assessment of the target. Thorough vendor preparation mitigates price chipping and keeps the process on schedule.

- Completion documentation including the SPA, SHA, earn-out arrangements, and escrow governs the transfer of ownership and the vendor’s post-transaction obligations.

- An experienced M&A advisor expands acquirer reach, enforces process discipline, and strengthens the vendor’s negotiating position at each stage of the transaction.

The 5 Steps at a Glance

| Step | Name | Objective | Timeline |

| 1 | Valuation & Preparation | Establish a defensible valuation basis | 4–8 weeks |

| 2 | Information Memorandum | Structure the investment case for prospective acquirers | 3–6 weeks |

| 3 | Buyer Outreach | Generate a competitive field of indicative offers | 4–8 weeks |

| 4 | Due Diligence | Support acquirer review; maintain transaction momentum | 6–12 weeks |

| 5 | Negotiation & Completion | Execute binding transaction documentation | 4–8 weeks |

Step 1: Valuation & Preparation

| approx. 4–8 weeks

Before approaching the market, vendors require clarity on two fundamentals: the strategic rationale for the transaction and a robust assessment of enterprise value. Both materially influence negotiating leverage throughout the process.

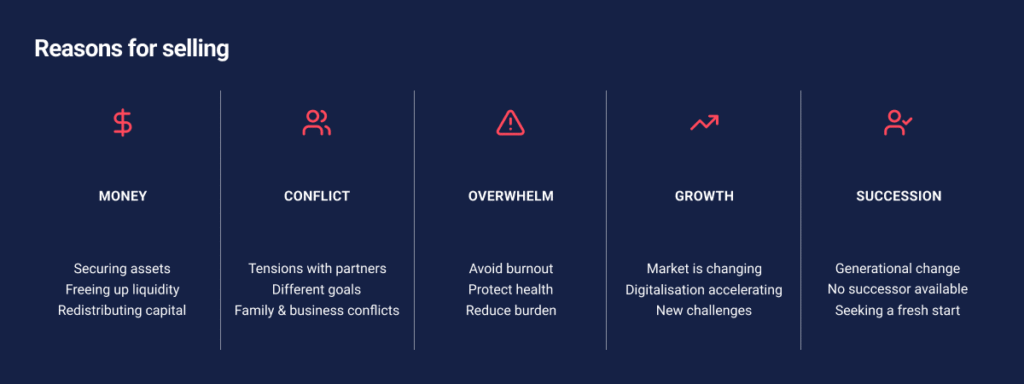

Why do you want to sell your business?

In our practice, we repeatedly see similar motivations for selling:

- Money: Entrepreneurs want to secure their wealth, create liquidity, or diversify their assets

- Conflict: With partners, employees, or within the family, requiring a new constellation

- Overwhelm: Burnout, health pressures, or management challenges that become too much

- Growth: Technological changes, new markets, or the need to secure the growth trajectory

- Succession: Generational change, lack of internal succession, or the sense that the business would be better positioned with a different partner

Once the motivation is clear, the actual preparatory work begins. The centerpiece of this phase is the financial derivation. You create an integrated financial model bringing together P&L, balance sheet, and cash flow. What remains is an adjusted EBITDA, the core of your operational earnings power.

| What is Adjusted EBITDA? EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortisation) represents the normalised operating profitability of the business. Adjustments remove non-recurring items and owner-specific costs such as above-market management remuneration or one-off exceptional charges to reflect the sustainable earnings base that an acquirer would inherit. Standard valuation methodology: Enterprise Value = Adjusted EBITDA × Sector Multiple Illustrative example: EBITDA of €2.0m × a multiple of 6.0x = Enterprise Value of €12.0m |

In parallel, a 3–5-year financial projection is prepared. Acquirers and their advisors will subject these forecasts to rigorous scrutiny; assumptions must be well-substantiated and clearly defensible. The result is a company valuation. Market multiples set the framework, but your growth potential, margin trends, and operational stability determine the final level. Those who complete this groundwork properly enter the market with realistic expectations.

Step 2: The Information Memorandum

| approx. 3–6 weeks

With enterprise value established, the next step is to present that value in a format that enables prospective acquirers to conduct a substantive initial assessment. The primary instrument is the Information Memorandum (IM).

What Is the Information Memorandum?

The Information Memorandum is the definitive marketing document in the sell-side process — typically 40 to 80 pages in length, professionally structured, and designed to support an acquirer’s decision to submit an indicative offer.

The Equity Story: Why Is This Business an Investment Case?

Put yourself in a buyer’s shoes: a potential investor is not just buying the past, they are also buying the future. The central question is therefore: why is this business attractive today, and why will it be even more attractive in five years?

Investors often think in two dimensions:

- Today: How strong is the business really? What has it already achieved?

- Tomorrow: How will it develop? Where are the growth levers?

A strong equity story connects both. It shows where your company creates value today through its market position, competitive advantages, and customer relationships, while making clear which levers will come into play in the years ahead.

The Information Memorandum: The Sales Document

The information memorandum is the central tool in this phase, essentially your sales pitch in document form.

The information memorandum distills four things

- Where you stand today: market position, business model, customer structure, how you generate revenue

- What you are worth: the value drivers and financial metrics that justify it

- Who leads you: your management team, their experience, and the organizational stability

- Where you are headed: the growth potential in the years to come

What happens in parallel?

While working on the information memorandum, you prepare the market outreach. You create a teaser for your shortlist, build a longlist of 20 to 50 potential buyers, and refine it down to a shortlist of 3 to 8 buyers. Simultaneously, you structure the data room, the digital foundation for due diligence, containing all key documents and contracts.

Are you considering selling your company?

Contact your Carlsquare Consultant today.

Step 3: Market Outreach, Finding the Right Buyer

| approx. 4–8 weeks

The information memorandum is ready, the shortlist of buyers is defined, and the shareholders are aligned. Now your company is brought to market in a targeted manner. The objective is to run a structured, competitive process that generates multiple indicative offers and maximises the vendor’s negotiating leverage.

Strategic Acquirers vs. Financial Investors

Strategic acquirers, typically corporates operating in the same or adjacent sectors, are motivated by synergy realisation: revenue enhancement, cost reduction, capability acquisition, or market consolidation. Where synergies are material, strategic acquirers frequently support higher valuation multiples.

Financial investors, primarily private equity funds, acquire businesses on the basis of stand-alone growth potential and target an exit within a five to seven-year investment horizon. They bring structured capital, operational expertise, and transaction execution capability.

The appropriate acquirer mix depends on the vendor’s strategic objectives. Both categories are capable of supporting a full exit. Vendors seeking to retain equity participation or influence over the business’s strategic direction post-completion will generally find greater structural flexibility with financial investors.

Making the Selection: How Do You Choose the Right Buyers?

Based on the indicative offers and conversations, you make a decision: which buyers proceed to due diligence?

The following criteria help:

- Valuation: Is the offer within an acceptable range for you?

- Structure: Does the proposed structure align with your goals and plans?

- Personal fit: Can you envision working with this buyer?

- Financing readiness: Does this buyer have the stability to actually close the deal?

The rule is simple: fewer buyers with genuine quality beats many with doubts. Typically, you proceed with 2 to 3 buyers into due diligence.

Step 4: Due Diligence

| approx. 6–12 weeks

Upon entering due diligence, you typically agree to negotiate exclusively with the selected buyers, meaning you do not engage with other interested parties during this phase. This is the point at which you commit. In return, the buyer gains access to all relevant information and has the time to thoroughly examine your business.

| What Is Due Diligence? Due diligence is the acquirer’s structured investigation of the target business, conducted across financial, legal, tax, and commercial workstreams. The process is designed to verify the representations made in the IM, identify material risks, and provide the evidential basis for confirming or adjusting the proposed transaction terms. |

Scope of the Due Diligence Process

- Virtual data room access: the acquirer’s advisory team reviews all material contracts, financial statements, corporate documentation, and operational records

- Third-party advisors: legal counsel, financial due diligence providers, and sector specialists conduct independent workstream reviews

- Management Q&A: detailed sessions addressing financial performance, strategic decisions, key risks, and operational dependencies

- Risk identification: findings are assessed for materiality and may give rise to purchase price adjustments, representations and warranties, or specific indemnities

Expected Outputs

- One or more binding, confirmed acquisition offers incorporating due diligence findings

- Negotiated transaction documentation including the SPA and, where applicable, the SHA

- A fully informed basis for selecting the final counterparty and proceeding to completion

Due diligence is consistently the most operationally demanding stage of the sell-side process. Historical financial data, management decisions, and contractual arrangements are subject to intensive scrutiny. Vendors who enter this stage with well-organised documentation and clear, consistent answers to anticipated queries are best positioned to maintain process momentum and protect transaction value.

Step 5: Contract Negotiation & Closing the Deal

| approx. 4–8 weeks

With due diligence concluded, all material transaction terms are negotiated and documented in final binding form: enterprise value, payment mechanics, representations and warranties, and the vendor’s post-completion obligations.

| Key Transaction Documents SPA (Share Purchase Agreement): the primary acquisition agreement governing the transfer of ownership, purchase price, completion mechanics, and seller warranties and indemnities. SHA (Shareholders’ Agreement): the shareholder agreement governing the rights and obligations of shareholders where the vendor retains an equity interest post-completion. Earn-out: a deferred consideration mechanism linking a portion of the purchase price to the achievement of defined financial or operational targets in the post-completion period. Escrow: a retention mechanism under which a portion of the consideration is held in trust as security against warranty claims for an agreed period post-completion. |

These documents govern not only the headline consideration but the vendor’s post-completion position in its entirety: ongoing management involvement, transition arrangements, and the commercial consequences of target underperformance.

Completion

Legal completion — effected through notarial execution of the transaction documents — marks the transfer of ownership and the formal conclusion of the sell-side process. For many vendors, this represents the culmination of months of sustained preparation, commercial negotiation, and personal commitment.

Completion marks the end of the transaction process and the beginning of the next phase of the business’s development under new ownership.

FAQ: Selling a Business

How long does a business sale take?

A professionally managed sell-side process typically requires 6 to 12 months from mandate commencement to legal completion. The precise timeline is a function of business complexity, sector dynamics, acquirer readiness, and the degree of vendor preparation at the outset.

When is the right time to sell a business?

From a transaction value perspective, the optimal window is one in which the vendor is not under pressure to transact. Vendors who approach the market from a position of operational and financial strength consistently achieve superior outcomes. Indicators of a favourable transaction environment include:

- Sustained EBITDA growth over the preceding two to three financial years

- Active M&A activity in the sector, reflecting strong acquirer appetite and competitive pricing

- Supportive debt financing markets, enabling acquirers to underwrite higher valuations

- A defined personal or shareholder timeline that makes the medium-term a natural transaction window

Conversely, vendors who approach the market under financial pressure, with deteriorating operating performance, or in circumstances where the motivation to sell is visible to the acquirer market, are materially disadvantaged in negotiations.

When is an M&A advisor worthwhile?

An M&A advisor is particularly valuable when:

- The vendor has limited or no prior transaction experience and is executing a sale process for the first time

- Managing a structured sell-side process internally would divert management attention from business performance

- The mandate requires access to an international acquirer universe beyond the vendor’s existing network

- The objective is to run a competitive process with multiple acquirers and maximise transaction tension

- The deal structure involves complexity — earn-outs, escrow arrangements, partial exits, or retained equity

Beyond acquirer access, an experienced M&A advisor brings process discipline at critical transaction junctures, substantive negotiation expertise, and the capability to insulate the vendor from the emotional pressures that characterise a complex sell-side process.

Can I sell only part of my business?

Yes. Minority stake disposals, majority transactions with vendor rollover equity, and phased exit structures are all well-established transaction formats. A partial sale may be an appropriate mechanism for realising liquidity while retaining participation in future value creation.

Does my business need to be profitable before a sale?

Not necessarily. While positive EBITDA is advantageous, acquirers ultimately underwrite forward-looking value. Businesses with negative or modest EBITDA may attract compelling offers where the strategic rationale, addressable market, and growth trajectory are sufficiently strong.

What happens if due diligence uncovers problems?

Due diligence findings frequently result in purchase price adjustments, enhanced warranty and indemnity provisions, or changes to the deal structure but rarely in transaction failure. A professionally managed process anticipates potential risk areas in advance, addresses them proactively, and ensures that identified issues are resolved within the negotiation framework rather than escalating to deal-breaker status.

Similar Insights