Head of Equity Research

Equity research CDON, Q2 2026: GMV leads, profits should follow

16 Jul 2026

Read the full report here:

CDON beat on GMV, but earnings missed our estimates, with the Q2 2026 shortfall largely explained by a lower take rate and higher marketing costs. The 2027 earnings inflexion thesis, however, remains largely intact, with operating leverage expected to kick in as growth initiatives mature.

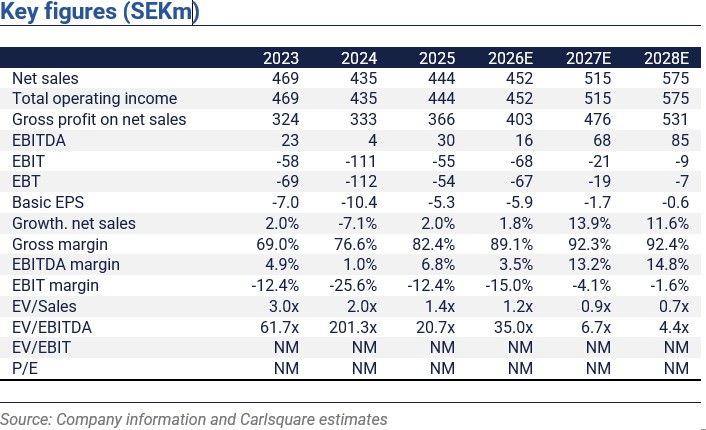

Growth trend in GMV continues, take rate is lagging

We believe the stronger-than-expected 13% increase in Gross Merchandise Value (GMV) in Q2 2026 reflects the marketplace’s ability to adapt to trends and seasonality rapidly. Also, the onboarding of new, larger European merchants (“giants”) is now well up to speed, with a clear positive effect on product supply and order volumes. We expect additional “giants” in the near future to help underpin growth. The impact of newly introduced EU tariffs on small parcels for Fyndiq is hard to predict. We expect higher sales (value) but lower take rates in the short term. In summary, double-digit GMV growth for the group also looks feasible in H2 2026, not least given that growth initiatives in marketing and SEO architecture have yet to play out. The take rate in the period was weaker than expected at 17.6% (18.4), burdened by the deliberate shift into faster-growing but lower-take-rate merchants and categories, as well as declining performance fees. As a result, we lower our near-term expectations for take rate and net sales. However, we expect an upwards trajectory from Q2 levels in H2 underpinned by the scaling of retail media advertising revenue and the planned phase-out of loss-generating 1P revenue.

Pressure from increased costs is mostly temporary

The EBITDA loss was wider than expected at SEK -7.3m (0.4), primarily due to a sharper decrease in take rate and higher marketing expenses than assumed. The latter expenses are mostly planned and/or temporary measures, including some SEK -3m in brand marketing costs related to an upcoming campaign. Also, the very strong growth and a recalibration of performance marketing algorithms inflated Fyndiq’s marketing costs in the quarter. On a positive note, the announced phase-out of the legacy 1P business will likely mitigate some of the pressure on take rates. CDON also foresees “operational leverage starting by the end of the year” and sticks to its target of close to SEK 100m EBITDA in 2027. Nevertheless, we adopt a slightly more cautious stance and review our EBITDA estimates for 2026 to 2028E downward by 17%. This is mainly in light of an expected flatter take rate development in the near- to medium-term.

Despite short-term margin headwinds, we still see significant potential

In the last 15 months, CDON has demonstrated a return to growth following a period of integration work subsequent to the 2023 merger. While margins will likely remain subdued in the current quarter, evidence of improved operating leverage towards the end of the year is a probable catalyst for higher valuation. In accordance with the changes to the estimate, we adjust our base-case valuation.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts Niklas Elmhammer and Markus Augustsson do not and may not own shares in the analysed company.

Ähnliche News