29 Apr 2025

Equity research, Svenska Aerogel Q4 2025: Momentum builds up for a breakthrough

30 Mrz 2026

Read the full report here:

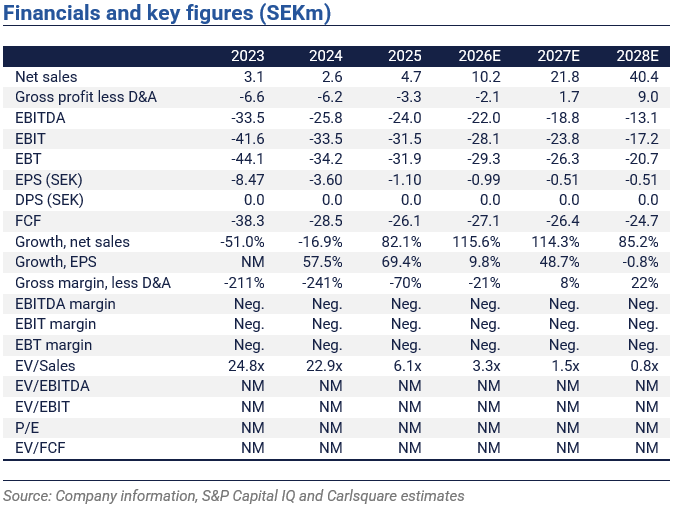

Svenska Aerogel closed 2025 with full-year revenue growth of 82% YoY, while from low levels. The net burn rate improved by SEK 6m, a meaningful step for a company still in commercialisation mode. With 15 customers in the commercial phase, a breakthrough year is approaching.

Solid growth alongside cost reductions

For the full year 2025, net sales increased by 82% to SEK 4.7m, marginally below our estimate of SEK 5.0m. The growth was driven by a maturing customer pipeline, the Advanced segment delivering larger recurring orders, alongside new traction in Building & Real Estate via European distributors.

EBITDA improved SEK 1.8m in 2025 to SEK -24.0m. Strip out the one-off benefit in 2024, when the Swedish Energy Agency loan was converted into a grant, and the underlying improvement was SEK 6.3m. COGS still run above revenues is a result of the early production ramp in Gävle. Cost cuts and top-line growth together reduced full-year net cash burn by roughly SEK 6m, which is meaningful amount at this stage. Operating cash flow came in at SEK -25.7m, an improvement of SEK 2.6m YoY, CAPEX was held to SEK 0.5m, and the company closed the year with SEK 8.3m in cash.

Momentum is building toward a revenue-breakthrough

With 15 customers now in the commercial phase, representing a 50% increase relative to 2024 and 2026 has the potential to mark a breakthrough year, underpinned by several converging catalysts. Matrix Brands’ product launch for a personal care product, expected mid-year, opens an entirely new end market. Outlast® and the North American customer are ramping recurring volumes, which are anticipated to grow materially over the coming periods. Over time, Saint-Gobain’s acquisition of Isoltech could unlock global scale for Quartzene® in lightweight concrete applications, a development that carries solid potential. In addition, Dekro Paints is approaching certification of a fire-retardant system in South Africa, adding a further growth vector. In summary, the trajectory is compelling with scaling revenues, a declining cost base, and an expanding sales-funnel.

Solid outlook creates potential upside, but financing risk lingers

While reiterating that the numerous near-term triggers remain a key consideration, the heightened financing risk should also be noted, especially given prevailing market conditions. In our model, the company will need SEK ~20m in external financing at latest in Q2 2026. We assume that a loan is granted by the larger shareholders, and a rights issue is carried out in Q1 2027. The associated risk/uncertainty is reflected in an increased discount rate. Thus, clarity around financing is another trigger.

Given the solid outlook for the year, we raise our net sales estimates for 2026E by ~13%. However, we lower our long-term gross margin assumption, which in turn reduces profitability at subsequent levels of the income statement. We revise our base-case fair value per share to SEK 2.5 over a 6-month horizon.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Ähnliche News