Head of Equity Research

Equity research Viva Wine Group, Q1 2026: Nordics shine in a slow market

11 Mai 2026

Read the full report here:

Viva’s business in the Nordics grew with improving margins, while profitability for Delta Wines floundered somewhat in a slow season. Despite uncertain markets and potential cost inflation ahead, the company signals it can protect margins. Organic growth and improved operating efficiency bode well for continued profit growth.

Organic growth and margin increase in the Nordics

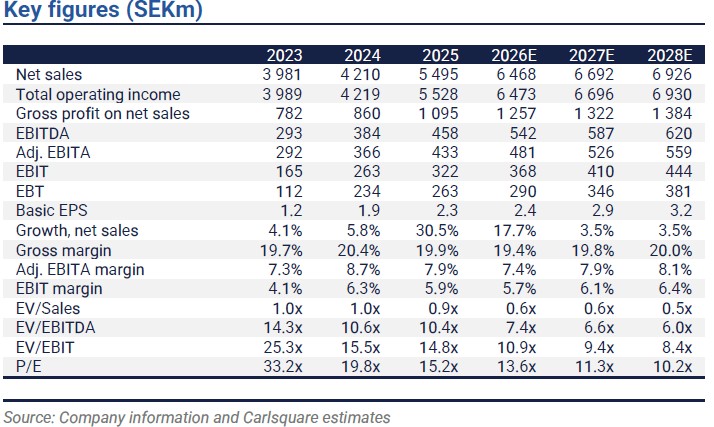

Viva Wine Group’s organic growth in Q1 2026, somewhat surprisingly, turned positive at two per cent, underpinned by solid sales performance across all Nordic markets. Also, price increases and a positive Easter effect contributed despite generally weak demand over the full quarter. Net sales amounted to SEK 1,351m, representing 51% growth, boosted by the acquisitions of Delta Wines and Alpha Brands. Our forecast for the quarter was SEK 1,367m. The deviation is due to a lower contribution from Delta Wines than we had assumed. The group EBITA margin at 5.5 per cent (5.6) was roughly in line with our expectations, as lower-than-expected profitability for Delta was mitigated by margin increases in the Nordics and the e-commerce business. Overall, Viva seems to perform better than its closest peers in the Nordics, building on its already strong market position and broad offering. Net sales for the B2C segment declined, but organic growth was 2 per cent. Our expectation was 3% growth. The EBITA margin increased to 5.8 per cent (3.8) due to lower operating costs.

Viva expects a stable gross margin despite expected cost inflation

The gross margin of 19.7 per cent (21.2) was in line with our expectations. Viva guides for a stable margin in 2026 (19.9 in 2025), as it expects a positive FX effect to offset higher freight costs driven by higher energy prices. Management also guides for OPEX to sales of 11-12 per cent in 2026E compared to 12.3 per cent in 2025. Viva says the first quarter provides a solid foundation for the rest of the year despite uncertainty regarding market development. The profitability outlook is better than we had feared, but we believe it is premature for us to pencil in a margin increase for 2026, given potential market headwinds.

Uncertain markets, but still room for earnings to continue to grow

We only make minor changes to our estimates following the Q1 2026 report. The organic growth is clearly encouraging. We expect markets in the current quarter to be volatile due to, e.g. the adverse Easter effect and uncertain consumer sentiment. Wine volumes were already down 19 per cent in April in Norway. We adjust our base-case valuation after peer multiples have turned lower and debt and minority shares have increased somewhat. We calculate that Viva Wine Group is still valued somewhat below its peers, with an EV/EBIT 2026E of 10.9x, compared to 11.5x.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts Niklas Elmhammer and Markus Augustsson do not and may not own shares in the analysed company.

Ähnliche News