29 Apr 2025

Equity research WPTG, Q1 2026: Platform momentum builds on all fronts

21 Mai 2026

Read the full research update below:

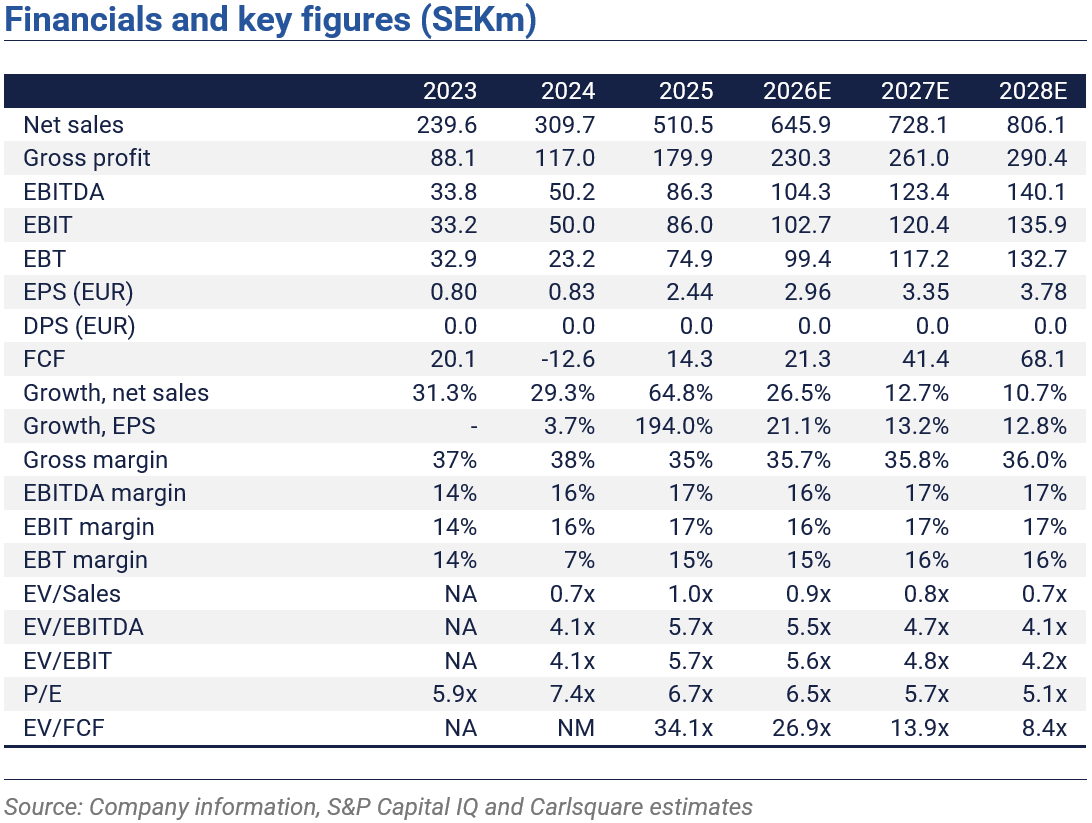

White Pearl delivered a solid Q1 revenue growth, with an estimated organic growth of ~26%. EBITDA was reported at SEK 23.4m, corresponding to a strong margin of 16.3%. Management has, encouragingly, raised the full-year 2026 revenue target. Whilst the operational momentum is clear, the share continues to trade at a discount.

Revenue up 45% with Europe emerging as a growth engine

With sales data for the quarter in place ahead of the report, net sales of SEK 143.7m came in broadly in line with our estimate. The growth rate YoY landed at a solid 45%, whilst we estimate the organic growth to ~26%. Europe accounted for over 25% of sales, up from 18% in H1 2025, underscoring the continued progress in building out the international revenue base. Gross profit of SEK 51.2m translated into a 36% margin, ahead of our 34% forecast, reflecting a more favourable revenue mix than we had anticipated.

EBITDA grew 48% YoY to SEK 23.4m, corresponding to a margin of 16.3%, against our estimate of SEK 24.3m. The modest shortfall reflects somewhat higher OPEX than anticipated, which absorbed the upside in the gross profit beat. EPS of SEK 0.71 came in 3% ahead of our SEK 0.69 estimate. Cash flow from operations was SEK -11.1m, weighed down by working capital movements, though we expect this to reverse in Q2. The cash balance stood at SEK 49.6m at the end of March.

Acquisitions accelerate and a raised revenue target

Organic growth proves the platform-model, while the M&A activity is high. On the back of this, management raised the 2026 revenue forecast to above SEK 620m, an 8.4% upward revision. Four acquisitions from Spotr Group were completed, adding Nordic software, cloud, and consulting capabilities. Post-period, WPTG acquired another Swedish company and the Bulgarian agencies CreateX and Native Digital, strengthening the European footprint. The pipeline remains active with LOIs for ServIT AB, Saltycustoms in Southeast Asia, GVO Media Group AB, Profit Solutions Sweden AB, and Guerilla Tactical Services in South Africa.

Lower multiples trim fair value despite solid fundamentals

We make only marginal adjustments to our estimates following Q1. Revenue forecasts are nudged up by an average of 0.3% across 2026-28E, whilst gross profit estimates are lifted by an average of 6.3%. EBITDA and EBIT estimates are broadly unchanged. Our revised fair value of SEK 29.0 per share (previously SEK 30.2), on a six-month horizon, is driven by softer EV valuation multiples in the broader market rather than any deterioration in the underlying business. At current levels, WPTG trades at a P/E NTM of 6.3x, a material discount to Nordic IT peers of ~54%. We consider this gap unwarranted as the platform model has demonstrated its ability to consistently generate organic growth at solid margins creating a credible outlook.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Ähnliche News