Managing Partner and Head of Debt Advisory

European Debt Markets: Quarterly Insights #2 2026

16 Apr 2026

Q1 2026 proved a challenging quarter for European debt markets, shaped by geopolitical uncertainty, rising stagflation fears, and a notable slowdown in issuance activity. Against this backdrop, we reflect on key developments shaping the leveraged lending and private credit landscape.

Key Insights:

- Leveraged Loan Issuance Contracts in Q1 2026

European leveraged loan issuance declined to EUR 22.7bn, the lowest first-quarter total since 2023, with geopolitical tensions and stagflation fears weighing on market activity. Direct lending volume fell 33% YoY to EUR 8.3bn across 35 transactions. M&A activity remained subdued but showed early signs of recovery at EUR 10.2bn.

- Pricing Divergence Emerging

Despite ongoing market volatility, lenders continue to price aggressively for quality assets. However, the spread differential between broadly syndicated loans and direct lending widened notably from 88bps in Q4 2025 to 168bps in Q1 2026, a dynamic borrowers and sponsors should factor into their financing decisions.

- Quarter Topic: HoldCo Financing – an effective instrument for additional leverage

With senior lenders becoming more conservative and exit timelines stretching, HoldCo PIK financing has moved firmly into the mainstream — including in mid-market deals below EUR 200m Enterprise Value. It enables sponsors to unlock additional leverage without affecting OpCo covenants, fund add-ons, and execute dividend recaps. All-in pricing ranges from c. 10–17%, with PIK compounding representing the key risk for borrowers.

European Debt Market – Q1 2026 Review

European leveraged lending activities

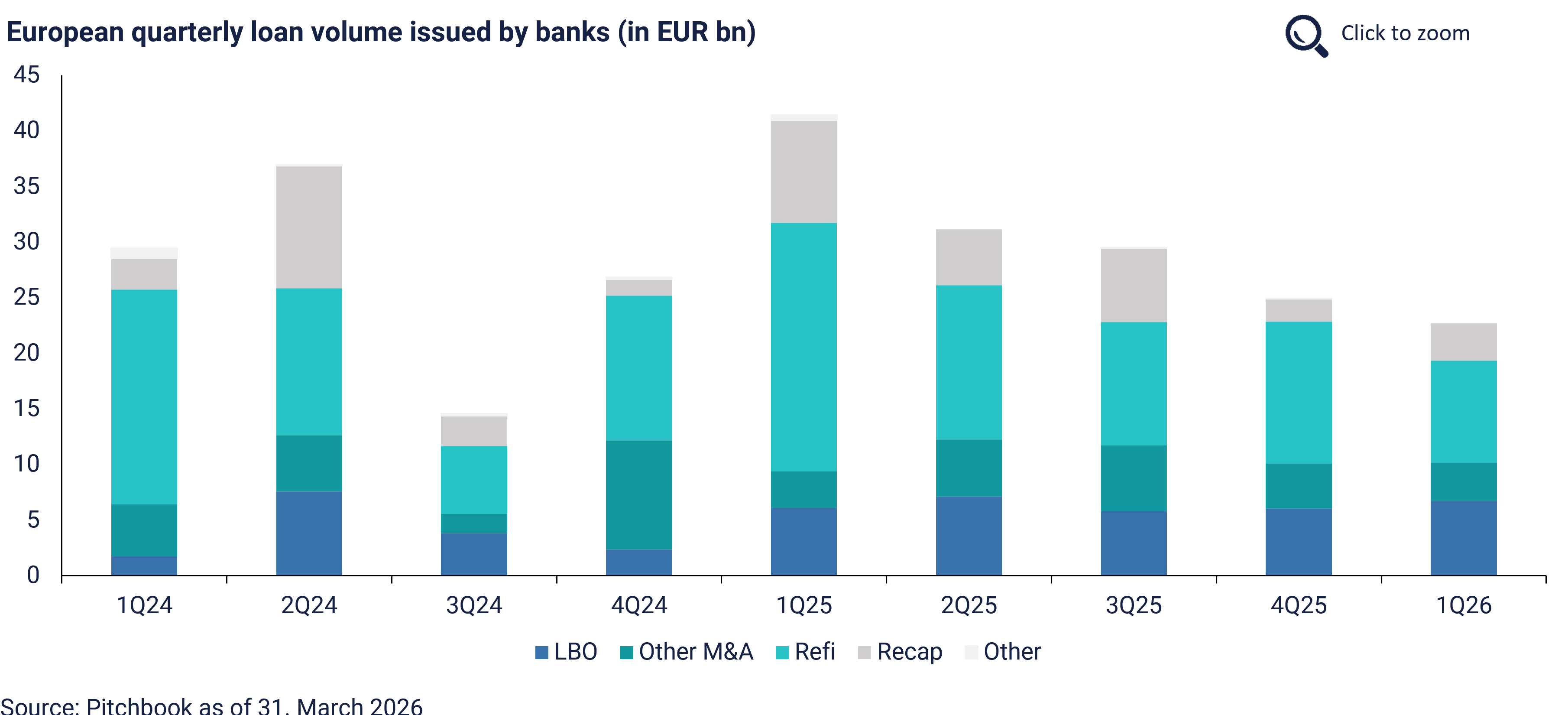

Leveraged loan issuance contracted in Q1 2026

The European debt markets faced significant headwinds in Q1 2026. On one hand, concerns grew around artificial intelligence and the systemic role of private credit in financing software business models. On the other, the outbreak of the war between Iran and the United States pushed oil prices higher, raising fears of stagflation and consequently surging higher financing costs. Market participants are now expecting 3 rate hikes in 2026 according to recent analysis conducted by Handelsblatt and Bloomberg¹.

Amid all this, leveraged loan issuance declined in Europe in Q1 2026 with a total value of EUR 22.7bn, representing the lowest first-quarter total since 2023, while 82% of this volume has been issued before the Feb. 28 commencement of airstrikes on Iran. Like last year, refinancing activity continued to represent the largest share of issuance by financing purpose, followed by LBO transactions. M&A activity — typically the primary driver of leveraged loan issuance — remained subdued but showed signs of recovery, with EUR 10.2bn of issuance being M&A-related. As market participants note, M&A pipeline is not absent, rather, processes have been stretched as investors are waiting for the market to stabilize mained moderate.

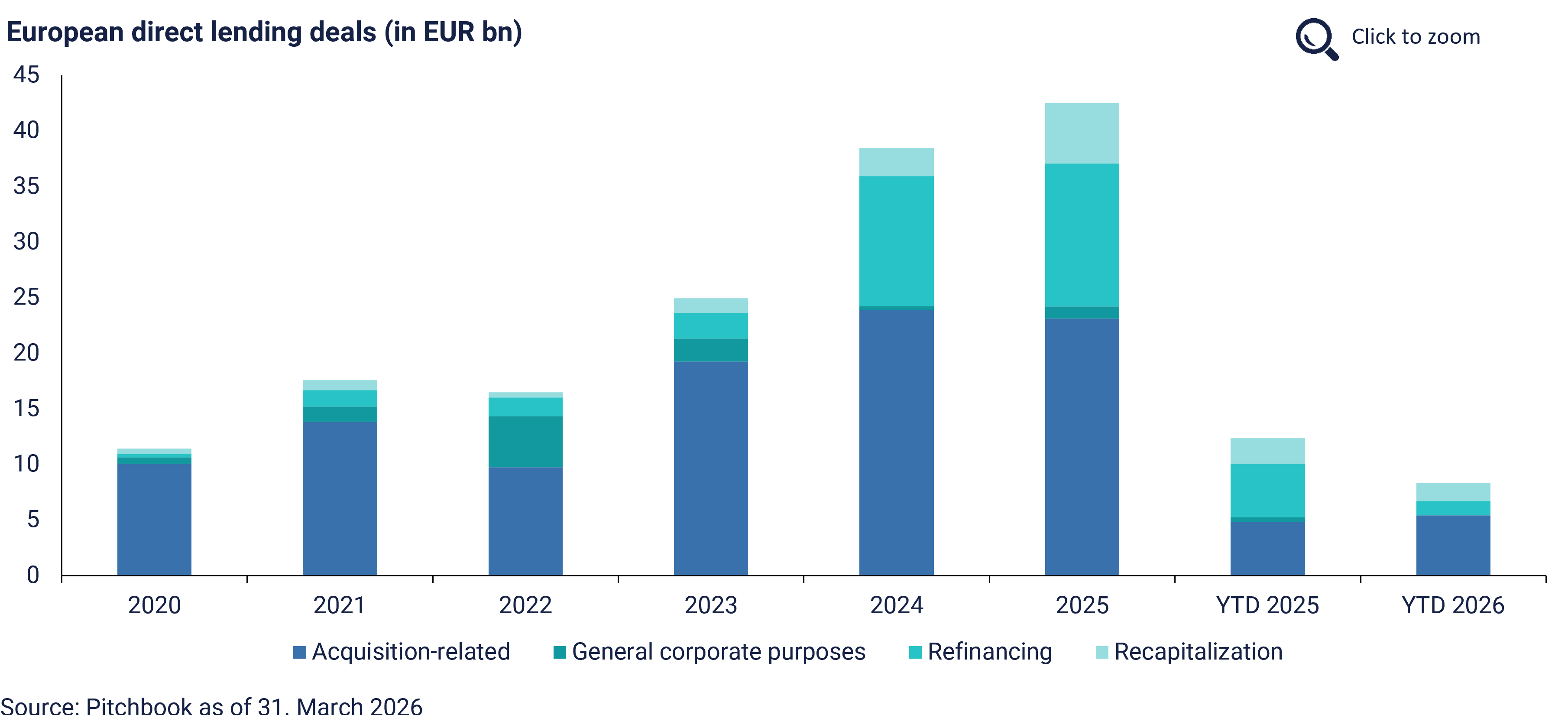

European direct lending volume reached an estimated EUR 8.3bn across 35 transactions in Q1/26, representing a 33% year-on-year volume decline and a 22% volume decline versus Q1 2025. Compared to the same YTD period of 2025, acquisition-related direct lending volume increased by EUR 0.6bn to EUR 5.4bn, while refinancing volume contracted from EUR 4.8bn to EUR 1.3bn. However, market participants point out that a number of transactions have been pending completion since last December.

Pricing remains compressed in Q1 2026 – but a divergence between bank and direct lending spreads is emerging

2025 and the early beginning of 2026 have taught that pricing has remained tighter than many market participants expected. Pricing continues to be somewhat constrained. Lenders are not yet demanding higher returns across the board in response to current conditions. Many still view the volatility as temporary and are willing to price aggressively for the right asset – balancing undoubted disruption to economic growth with the reality that this will likely mean even fewer processes launching and a correspondingly more competitive environment for the better-quality assets.

However, the divergence between broadly syndicated loan (BSL) and direct lending spreads is signaling an emerging, albeit modest, widening of spreads. According to LCD data, the average spread differential between the two markets for sponsored acquisition financing was 168bps in the first quarter of 2026, up from just 88bps in Q4 2025. Direct lenders are holding their pricing while the BSL market through banks continues to tighten — a gap that borrowers and sponsors should factor into their financing decisions.

Outlook on interest rate environment

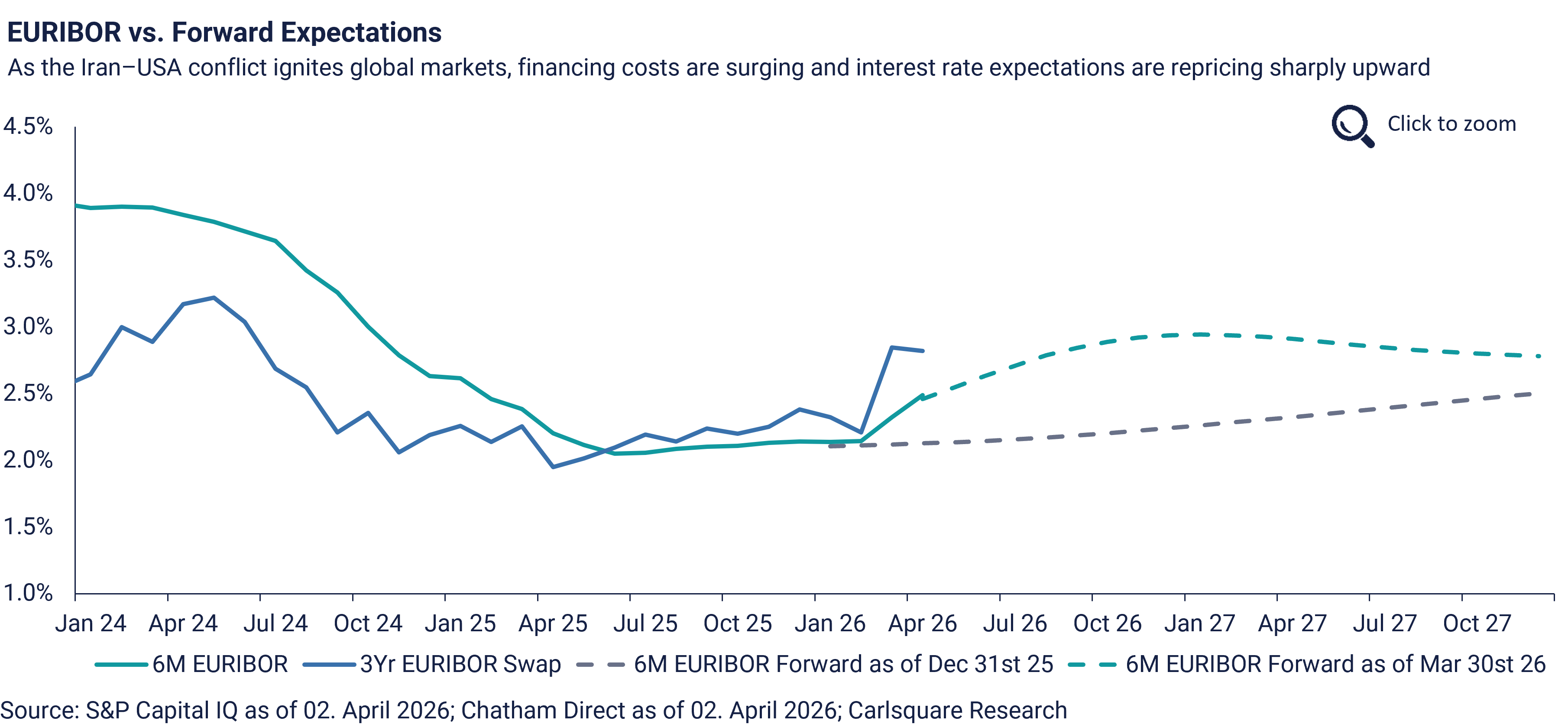

The ECB held rates unchanged at their latest meeting in March at 2.0% since June 2025 but warned equally that soaring energy prices due to ongoing war in Ukraine and newly outbreak of the Iran war would have a material impact on inflation. The ECB is expecting the inflation rate to be at 2.6% for this year compared to a previous estimate of 1.9% in December 2025. Likewise, the Bank of England decided in their most recent meeting to keep the interest rate steady at 3.75%. As illustrated in the Carlsquare Euribor vs. Forward Expectations chart, a comparison of forward curves at end-2025 and end-March 2026 reveals that markets have already priced in close to 80 bps of near-term risk with three interest rate hikes this year, reflecting a notable increase in uncertainty among market participants.

Private Credit: Stress Test, Not Crisis

Private credit has rarely been out of the headlines this quarter. While much of the noise has originated in the US, the implications are acutely relevant for European markets, where direct lending has grown rapidly in recent years and some (but far from all) of the same dynamics apply.

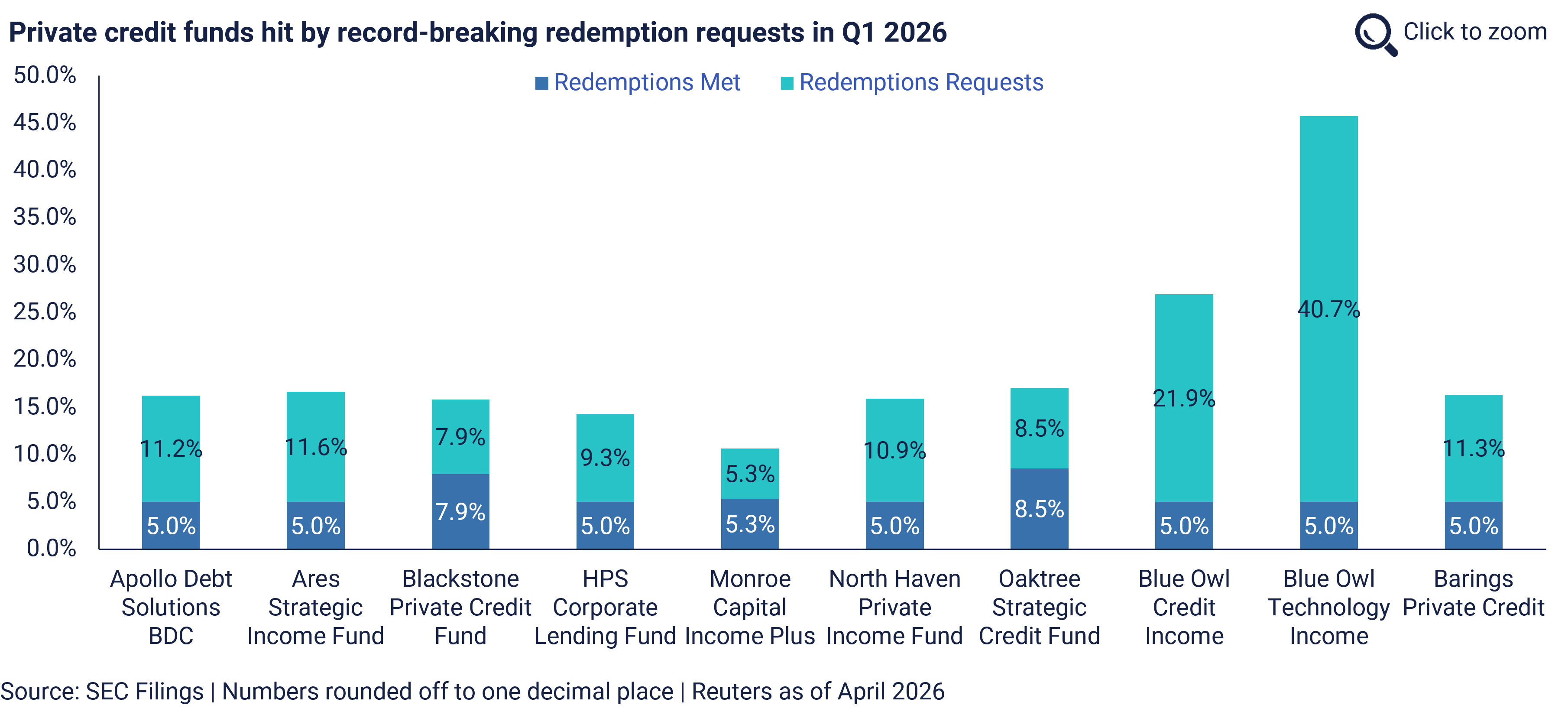

So what is actually happening? The global private credit asset class has grown from roughly USD 300bn in 2010 to USD 3.5tr by end-2024. It is now facing its first real test. Over USD 20bn in redemption requests have hit US based funds, with seven large managers “gating” (or, restricting) outflows², Moody’s revised its BDC outlook to negative, and the sector recorded its first-ever quarterly net outflow. In response, private credit managers have unsurprisingly seen their shares sell off sharply, with leading names down more than 25% (some more than 50% from their peaks).

It is worth noting here that redemption requests have been at “semi-liquid” vehicles – particular funds designed to offer investors periodic liquidity windows, unlike traditional closed-end private credit funds where capital is locked up for the life of the investment. The core, closed-end market – which is prevalent in European Direct Lending – has been largely unaffected.

Notwithstanding the broader resilience of leveraged lending, modest AUM declines and falling credit manager share prices point to some unease in the Private Credit space. The issues are, in our view, less about defaults or credit quality deterioration; rather, they centre on transparency — and how investors are now looking at loans underwritten at high leverage multiples during the peak years of 2021 and 2022, where equity cushions have since compressed and some borrowers have switched to payment-in-kind interest. The key investor question — how would these loans price if written today? — is not easy to answer in a market with essentially no secondary trading, and it is that uncertainty, rather than fundamental credit deterioration, driving the redemption pressure.

Stepping back, this is better understood as a symptom of an asset class maturing at a particularly challenging moment. Incubated in a zero-rate world that no longer applies, Private Credit now faces slower deal flow, abundant competing dry powder, and banks across Europe visibly re-engaging with the middle market. The era of rapid AUM growth is likely behind us, and consolidation feels increasingly inevitable — though none of this amounts to a re-run of the global financial crisis; just an asset class that must work harder to justify its liquidity and transparency trade-offs to investors.

Stay up to date with relevant Debt News by subscribing to quarterly newsletter.

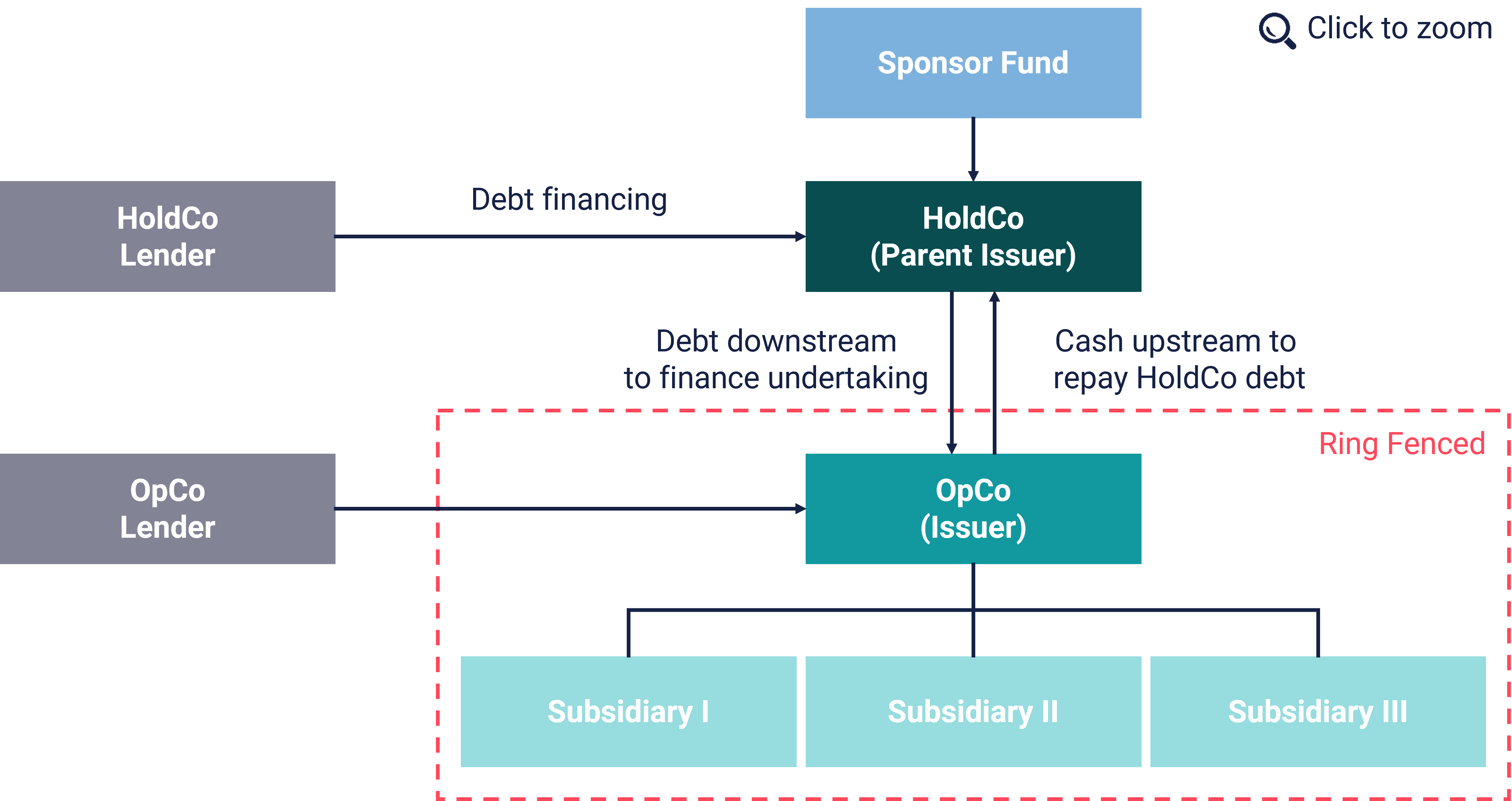

Quarter Topic: Hold Co Financing

HoldCo Financing – An effective instrument for additional leverage

Interest rates have stayed higher for longer. Exit timelines have stretched. Senior lenders have become more conservative. In this environment, HoldCo financing has moved firmly into the mainstream — across both the private credit and public debt markets. It is now appearing with increasing regularity in mid-market financings — deals below EUR 200m enterprise value — where it was rarely seen five years ago.

In this quarter’s newsletter, we introduce this financing instrument as a potential solution for additional leverage. A solution that the team at Carlsquare Debt Advisory has already successfully arranged to secure growth financing for ENTRO Invest GmbH and VM Capital.

What is HoldCo financing?

In HoldCo financing structures, the debt is lent to a holding company (“HoldCo”) that sits typically one layer above the operating entity (“OpCo”) and which is then down-streamed as cash injection to the OpCo. This lending does not cause any complications for the OpCo since the credit documentation allows it and the financial metrics and maintenance covenants are not affected by the new lending to the HoldCo. The repayment of the debt effectively relies on upstream distributions from the operating business or on exit proceeds.

Which debt instruments are used?

The debt instruments used in these situations are loans that are structurally subordinated to the debt from the OpCo and usually include a PIK toggle – also known as HoldCo PIK loans. The PIK allows the borrower to switch between cash-pay and compounded interest (“PIK”) at set intervals, though toggling typically triggers a pricing step-up.

Why has it gained popularity?

HoldCo financings allow portfolio companies of private equity sponsors to raise more capital when the debt capacity on the OpCo level is utilized already (i.e., HoldCo debt is net leverage neutral to the OpCo debt). They also reduce the sponsor’s equity contribution as a source of capital for the acquisition consideration, at a time when lenders to the OpCo are requiring more favorable loan-to-value ratios. Another advantage is that the HoldCo debt, in case forwarded as cash injection to the OpCo, keeps more cash in the operating business for growth purposes, e.g. financing add-on acquisitions and supporting the overall business strategy of the portfolio company. Lastly, it is also an effective tool for sponsors to extract a dividend payment from the company (recapitalization) while the credit documentation on OpCo level usually does not allow for it.

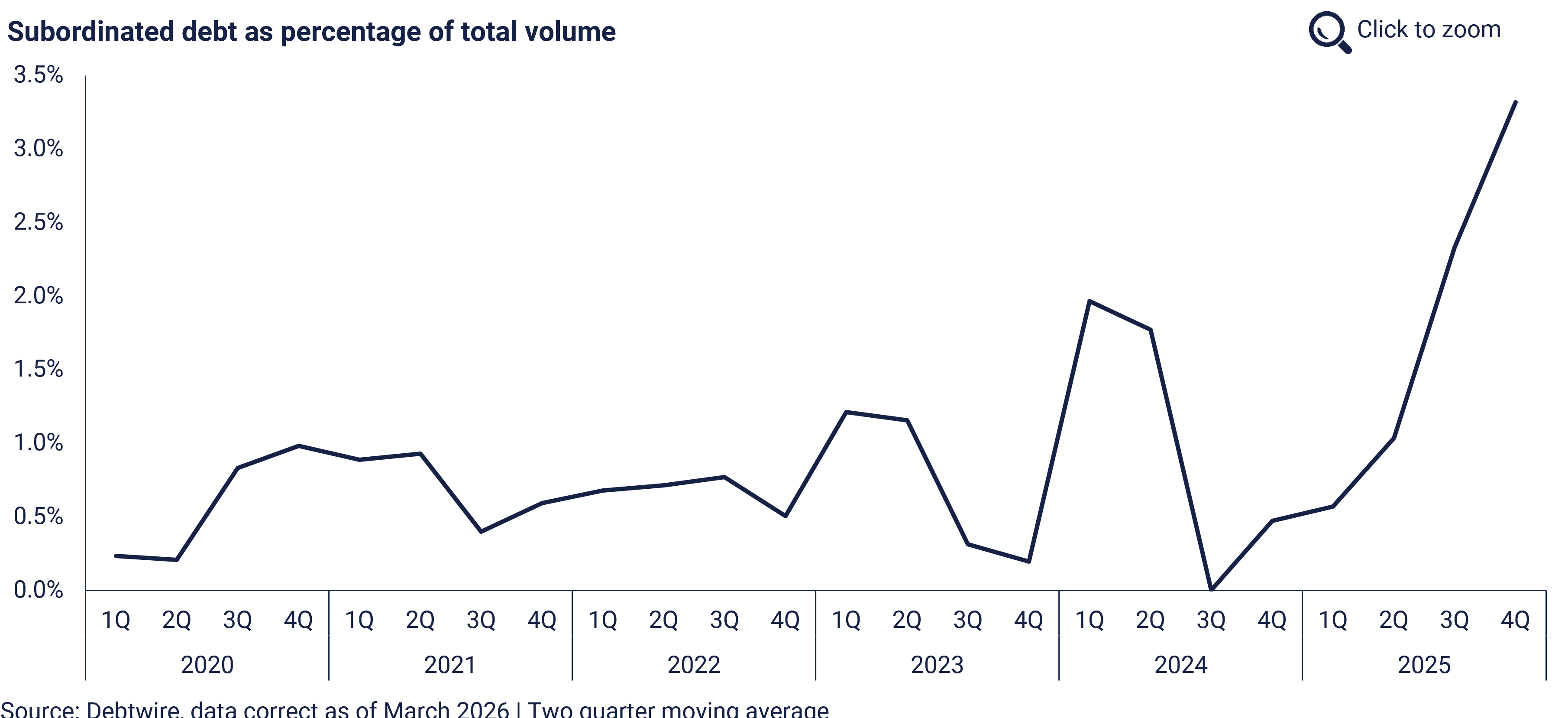

Recent market data from Debtwire indicate elevated activity in subordinated debt markets throughout 2025³. Subordinated bonds saw particularly notable increase in issuance volumes, rising to 3.32% of total volume in Q4 2025 vs. 0.57% in Q1 2025. PIK loans have also surged, accounting for approximately 11% of capital deployed by direct lenders in Q3 2025 – underscoring a broader shift toward flexible, non-cash pay financing structures according to Debtwire.

Who provides the HoldCo financing and what are the costs?

Private credit funds are the primary providers of HoldCo financing in Europe. The lender universe is narrower than that of OpCo debt — borrowers should expect more negotiation on documentation and, in some cases, equity participation or warrant coverage as part of the overall financing package as significant call protection (required min. returns of lenders are higher). All-in pricing in the current European market falls broadly in the 10–17% range, depending on structure, leverage (“look- through” net leverage, LTV), and asset quality. Call protection is standard — lenders providing deferred-cash instruments expect to be compensated if the borrower refinances early.

What are the risks and complexities?

- For borrowers — compounding could work against you.

- Repayment at maturity may greatly exceed the original principal. A 15% PIK loan of EUR 20m can grow to about EUR 40m in five years. Longer holding periods increase this amount, which is prioritized over equity in the payment waterfall.

- Holdco debt typically lacks leverage-based financial covenants, but lenders may require a pro forma leverage test to avoid excessive leverage. Leverage test includes HoldCo debt and earnings throughout the corporate structure, unlike OpCo-level test which excludes HoldCo debt.

- For lenders — structural protection is everything.

- HoldCo lenders are typically unsecured and ranked below OpCo creditors, with HoldCo as the sole obligor. Occasionally, HoldCo financing is secured by a share pledge in HoldCo.

- OpCo lenders set dividend blockers and payment restrictions, limiting cash flow to HoldCo. In stress situations, these can halt upstream distributions, making HoldCo lenders rely solely on exit proceeds for recovery.

Summary – HoldCo financing

An effective tool for additional leverage while preserving cash at OpCo level: It avoids immediate cash interest burden at the operating company—relevant when free cash flow is tight or reinvestment needs are high. Uses cases:

- Mid-hold liquidity bridge: With longer holding periods, PIK can bridge capital needs for growth or liquidity management.

- Add-ons without reopening senior terms: HoldCo PIK can fund bolt-on acquisitions without renegotiating the senior debt package.

- Dividend recap / LP liquidity: Depending on structure, can create “top-of-structure” liquidity without increasing OpCo cash interest.

- Closing valuation gaps: Junior/non-cash-pay tranches can help buyers reach higher valuations while keeping deal economics workable.

Sources

(1) Inflation: Der Iran-Krieg erschüttert das globale Zinsgefüge

(2) Barings caps withdrawals at private credit fund after redemption requests spike | Reuters

(3) Lenders get creative with junior capital as menu of options grows | ION Analytics | Debtwire

For any questions feel free to reach out to our authors Daniel Gebler, Head of Debt Advisory (Germany), Constantin von Wiedersperg, Director (Germany), and Andrew Hamilton, Director Debt Advisory (United Kingdom).

Similar Insights