29 Apr 2025

Equity research Svenska Aerogel, Q1 2026: Rights issue and focus on upcoming catalysts

29 Apr 2026

Read the full research update here:

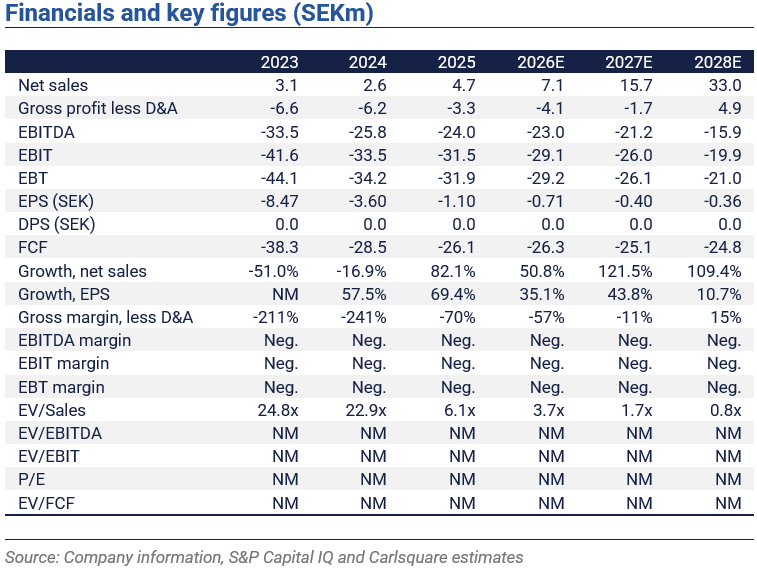

Svenska Aerogel reported net sales of SEK 1.1m in Q1 2026, somewhat below our estimate. EBITDA of SEK -5.8m was, however, ahead of our forecast, driven by tight cost control. The 2026 catalysts remain intact, while the company executes a capital raise.

Cost discipline and a capital injection

Revenue and order intake have yet to scale in any meaningful way, which is in line with our expectations. In Q1 2026, net sales came in at SEK 1.1m, down 18% YoY and 12% below our forecast. Given the low revenue base, the variance was immaterial in practice. Tighter OPEX control, however, lifted EBITDA to SEK -5.8m, an improvement from SEK -6.6m in Q1 2025 and 9% ahead of our estimate. FCF came in at SEK -5.6m, with minimal capex. Cash at quarter-end was SEK 3.6m.

Shortly ahead of the Q1 report, the company announced a rights issue of units, with each unit comprising two shares plus a free-of-charge warrant (TO9). The subscription price is set at SEK 1.86 per unit, equivalent to SEK 0.93 per share. The subscription period is preliminarily scheduled for 29 April to 13 May 2026. Assuming full take-up, the company will raise net SEK ~17.8m. Of the proceeds, 54% is earmarked for sales and marketing, with the remainder intended to fund continued product and application development. The company states the issue covers its funding needs through to the end of Q1 2027. In addition, potential gross proceeds of ~SEK 9.2m could be added from TO9.

Full-year 2026 catalysts remain intact

The company has 15 customers in the commercial phase, with an aggregate volume potential of c.450 tonnes per year, and a project pipeline of 170 ongoing customer projects. The distribution network is being broadened via KRAHN Chemie in Germany, while new opportunities are opening up as the company’s material is being evaluated in the EU defence research project CATHERINA. Matrix Brands’ launch of a personal care product, expected around mid-year, stands out as the clearest near-term revenue catalyst for Quartzene®. Meanwhile, Outlast Technologies continues its ramp-up and remains central to the full-year view.

Clear potential upside versus the subscription price

Following the Q1 outcome, we cut our revenue forecasts for 2026–2028E by ~8% on average, reflecting a slower initial revenue ramp. This does not change our view on Quartzene®’s market potential. Based on our revised forecasts, higher funding risk, and the equity raise with associated dilution, we lower our base case fair value to SEK 1.5 per share (2.3).

Our fair value still implies clear upside versus the issue subscription price per share, driven by continued cost discipline and accelerating commercial momentum in H2 2026. Near-term risk remains high given uncertainty around the outcome of the capital raise. A positive outcome would materially reduce funding risk and thus, strengthen the case.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Ähnliche News