Senior Equity Analyst

Equity research CDON Q2 2026: First impression – Solid GMV while growth investments weigh on margins

15 Jul 2026

Today, CDON AB published its interim report for Q2 2026. Below are our first impressions of the outcome, including deviations from our estimates.

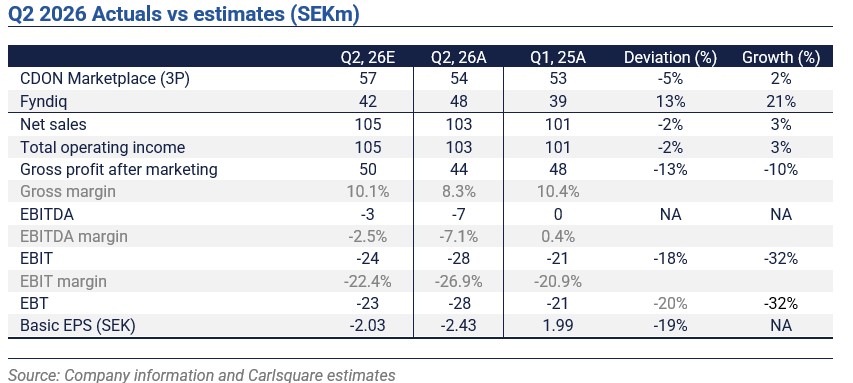

Gross Merchandise Value (GMV) grew in the double digits, once again stronger than expected, driven by high volumes in categories such as Home Electronics and Sports and Outdoor. However, the take rate fell more than expected as a mix shift into faster-growing but lower-margin merchants and categories weighed on net sales. Margins were lower than expected as marketing costs increased to 9.3% (8.0) of GMV largely driven by strategic front-loaded growth initiative costs in, e.g., brand marketing.

- For Q2 2026, CDON AB reported a Gross Merchandise Value (GMV) of SEK 521m, corresponding to a 13% increase, a similar strong rate as the previous quarter. Our forecast was SEK 491m. The main positive deviation was in the Fyndiq segment. Due to a lower take rate, net sales increase was limited to 3%, slightly below our expectations.

- EBITDA decreased to SEK -7.3 (0.4), compared to our forecast of SEK -3m. The difference from our estimates is a lower take rate and higher marketing costs than assumed.

- Cash flow from operations increased to SEK 50m (10) from improved working capital.

Growth has been stronger than expected. However, we will likely need to review our assumed trajectory for take rate and margins somewhat going forward. At the same time, we expect operating costs relative to sales to normalise in 2027, supporting an improvement in profitability.

The company will host a presentation of the Q2 2026 interim report at 10 am today. We intend to provide a research update on CDON AB shortly. Read our latest update here.

Disclaimer

Carlsquare AB, www.carlsquare.se, hereinafter referred to as Carlsquare, is engaged in corporate finance and equity research, publishing information on companies and including analyses. The information has been compiled from sources that Carlsquare deems reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be considered a recommendation or solicitation to invest in any financial instrument, option, or the like. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for either direct or indirect damages caused by decisions made on the basis of information contained in this analysis. Investments in financial instruments offer the potential for appreciation and gains. All such investments are also subject to risks. The risks vary between different types of financial instruments and combinations thereof. Past performance should not be taken as an indication of future returns.

The analysis is not directed at U.S. Persons (as that term is defined in Regulation S under the United States Securities Act and interpreted in the United States Investment Companies Act of 1940), nor may it be disseminated to such persons. The analysis is not directed at natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign laws or regulations.

The analysis is a so-called Assignment Analysis for which the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published on an ongoing basis during the contract period and for the usually fixed fee.

Carlsquare may or may not have a financial interest with respect to the subject matter of this analysis. Carlsquare values the assurance of objectivity and independence and has established procedures for managing conflicts of interest for this purpose.

The analysts Markus Augustsson and Niklas Elmhammer do not own and may not own shares in the analysed company.

Similar News