17 Jul 2026

Equity Research White Pearl Technology Group, Q1 2026: Revenue beat confirmed, margin quality in focus

20 Apr 2026

Read the full preview on the link below:

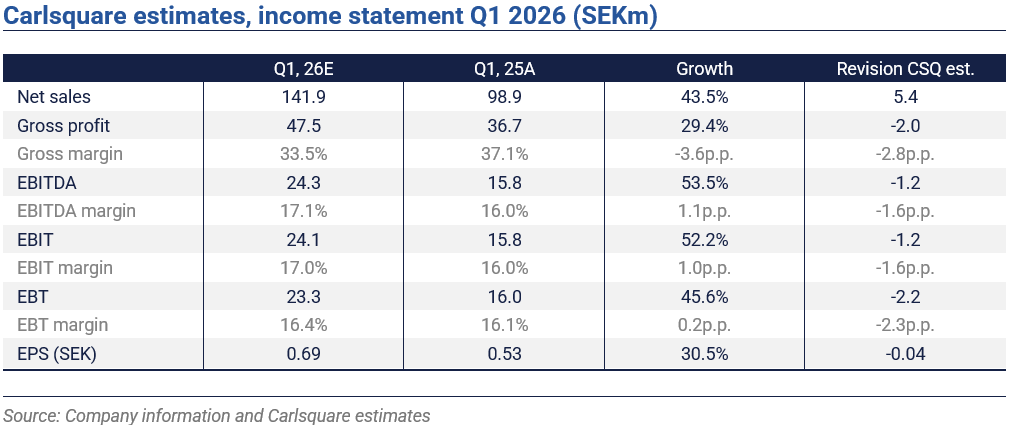

White Pearl Technology Group (WPTG) reports Q1 2026 on 20 May. Preliminary sales are already out, with net sales of SEK 141.9m, up 43.5% YoY. That is a SEK 5.4m (4.0%) beat versus our mid-March estimate, though it landed in line with management’s prior guidance. We estimate organic growth for the quarter to a solid 20-25%, broad-based across core markets per the company’s own commentary.

Management has guided that Q1 acquisition activity will begin contributing more meaningfully from Q2. That points to a to a somewhat stronger revenue base heading into H2, consistent with the group’s reiterated FY 2026 revenue target of SEK ~620m. Meanwhile, the M&A pipeline stays active. Beyond LOIs signed for ServIT (Sweden) and Saltycustoms (Malaysia and Singapore), a non-binding LOI was recently signed with Profit Solutions Sweden AB, a cash-flow-positive digital marketing agency doing roughly SEK 13.5m in annual revenue.

Two areas to watch at the Q1 print are management colour on the pace of gross margin recovery post Q4 2025, and the trajectory of European revenues, which accounted for more than 30% of group sales in February 2026 and continues to build. We have trimmed our Q1 EBITDA estimate marginally to SEK 24.3m (17.1% margin), reflecting a somewhat lower gross margin than previous, tied to an assumed high activity at Lumin4ry. Our estimate still implies 53,5% EBITDA growth YoY, reflecting scalability.

Ahead of the report, we marginally revise our fair value per share to SEK 30.1 (29.9), partially due to higher valuation multiples in the market. Our fair value corresponds to an implied NTM P/E discount of ~25%. The share is currently trading at a ~66% discount, framing the investment opportunity.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Similar News