Senior Equity Analyst

Equity research Zinzino Q1 2026: Solid operating leverage

25 May 2026

Read the full report here:

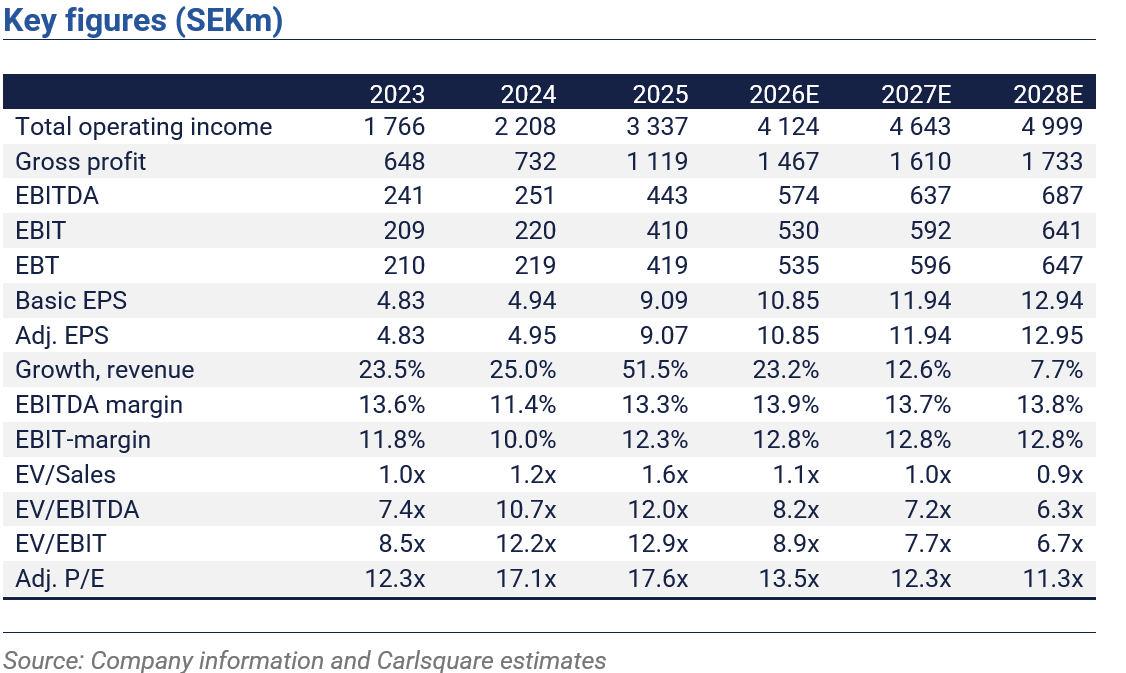

We are encouraged by the strong profitability, supported by a 5 percentage-point improvement in gross margin in Q1 2026. Also, we estimate that the underlying growth held up better than anticipated, further driving scalability. We raise our earnings forecasts as a result.

Sales growth in line, however, “better mix” than assumed

In line with the preliminary sales pre-announcement in April, Zinzino reported 26 per cent revenue growth in Q1 of 2026. The main regional drivers of absolute sales were again Central Europe and North America. While organic growth appears to have slowed somewhat, we believe the underlying growth rate, adjusted for FX and acquisitions, remains above our revised expectations. Conversely, the revenue impact from recent acquisitions, e.g., It Works! appears less than we had previously assumed. In that regard, we interpret that Zinzino also lowered its expectations for revenue contribution from It Works! for 2026. Overall, however, we believe the growth mix is reassuring on the back of somewhat slower total sales growth reported in recent monthly preliminary sales reports.

Higher gross margins provide operating leverage

Margins were again clearly higher than our forecast and Zinzino’s financial targets. This was primarily due to stronger gross margin expansion than we had assumed. Year over year, the gross margin increased by 5.1 percentage points to 37%, above our forecast of 35.5%. A weaker USD and lower raw material costs were the main drivers. At the same time, operating expenses increased largely in line with our expectations. Bottom line, EBITDA increased to SEK 142m (78), corresponding to a margin of 15.4%. Our estimate was SEK 130m, corresponding to a 14.2% margin. Management sees some inflationary impact, e.g., from increased freight costs going forward. On the other hand, the integration of acquisitions appears to run smoothly. In sum, we still expect somewhat lower margins sequentially in the coming quarters; however, the Q1 outcome boosts our FY2026 expectations.

Margin trend supports a raised base case valuation

We have adjusted our sales estimates somewhat (-2 per cent on average for the forecast period) due to a lower expected contribution from acquisitions than in our previous forecasts. We assume slightly below ten per cent organic growth for 2026 vs an estimated >30 per cent in 2025. At the same time, we adopt a more optimistic view regarding gross and EBITDA margins. As a result, we increase our EBIT forecasts by about 10 per cent over the near- and medium-term. The updated forecasts support the DCF valuation and offset dilution from share-based payments in acquisitions.

Disclaimer

Carlsquare AB, www.carlsquare.se, hereinafter referred to as Carlsquare, conducts business with regard to Corporate Finance and Equity Research in which areas it, among other things, publishes information about companies including analyses. The information has been compiled from sources that Carlsquare considers to be reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or the like. Opinions and conclusions expressed in the analysis are intended only for the recipient.

The content may not be copied, reproduced or distributed to another person without the written approval of Carlsquare. Carlsquare shall not be held responsible for any direct or indirect damage caused by decisions made on the basis of information contained in this analysis. Investments in financial instruments provide opportunities for value increases and profits. All such investments are also subject to risks. Risks vary between different types of financial instruments and combinations of these. Historical returns should not be considered as an indication of future returns.

The analysis is not directed to US persons (as defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Company Act 1940) nor may it be disseminated to such persons. The analysis is also not directed to such natural and legal persons where the distribution of the analysis to such persons would result in or entail a risk of a violation of Swedish or foreign law or constitution.

The analysis is a so-called Commissioned Research Report where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published on an ongoing basis during the contract period and for a usual fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values the assurance of objectivity and independence and has established procedures for managing conflicts of interest for this purpose.

The analysts Niklas Elmhammer and Markus Augustsson do not own and are not allowed to own shares in the company analysed.

Similar News