Senior Equity Analyst

Equity research CDON AB Q1 2026: Building on solid growth momentum

24 Apr 2026

Read the full report here:

CDON once again demonstrated double-digit growth, helped by new merchant onboarding, despite some issues with marketing channels. The focus is on implementing initiatives that should support continued growth and gradually help improve underlying profitability.

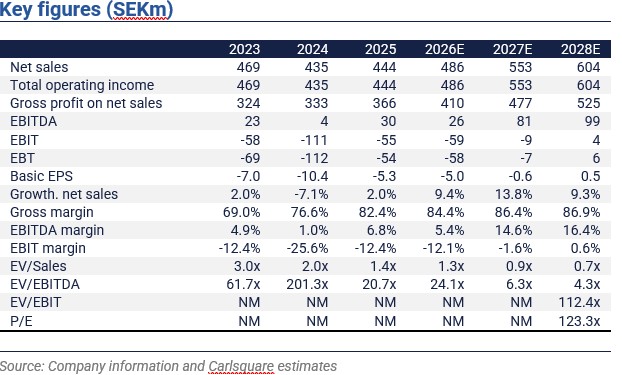

GMV and net sales outperform our expectations

The solid growth momentum for CDON continued in Q1 2026, as Gross Merchandise Value (GMV) and net sales increased by 14% and 13%, respectively, at similar rates to the previous quarter. Our revised forecast was mid-single-digit increases. The beat follows continued higher-than-anticipated orders and average order value, as well as good traffic growth (according to our research). The onboarding of new European merchants was successful, as their share of GMV increased from 2 to 5% during the quarter. Take rate was stable despite some headwinds in product and merchant mix. While the macro outlook has arguably turned more uncertain, we believe recent quarters indicate CDON is gaining share in the Nordics, supporting growth momentum. All in all, we only make small adjustments to our GMV and net sales estimates following the report.

Growth initiatives and marketing hamper margins in the short term

The EBITDA loss was slightly narrower than expected at SEK -2.8m (0). To some extent, this was explained by high merchant performance fees in the Fyndiq segment, which will likely normalise going forward. CDON says it is on track with implementing the growth initiatives announced in the Q4 report. The reported impact on OPEX and CAPEX was limited during the period and mostly related to a tech resources boost to increase development efficiency, e.g., through agent coding, and scaling the retail media offering. The latter is aimed at increasing the take rate by improving advertising revenue from group sites starting Q2. However, we expect advertising revenue to remain modest initially and, to a large extent, be absorbed by increased brand marketing costs in the Nordic markets outside Sweden as part of the announced growth initiatives. In sum, we lower our margin assumptions somewhat in the short to medium term, reducing EBITDA forecasts by 4% on average for 2026-2028E. However, we still assume solid operating leverage in 2027, underpinned by GMV expansion and, eventually, higher take rates.

Good prospects for gradually improving profitability

The recent quarter further demonstrates that CDON is back on the growth track, supported by investments and growth initiatives gradually implemented since the 2023 merger of CDON and Fyndiq. It is the clearest sign so far that CDON is starting to unlock the potential of the e-commerce marketplace. However, as explained above, increased marketing and technology development will weigh on reported margins in 2026 in line with the company’s plan. Still, we believe CDON will show improved underlying profitability in the coming quarters if growth momentum holds. Following updated forecasts, we adjust our base case valuation slightly.

Disclaimer

Carlsquare AB, www.carlsquare.se, hereinafter referred to as Carlsquare, is engaged in corporate finance and equity research, publishing information on companies and including analyses. The information has been compiled from sources that Carlsquare deems reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be considered a recommendation or solicitation to invest in any financial instrument, option, or the like. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for either direct or indirect damages caused by decisions made on the basis of information contained in this analysis. Investments in financial instruments offer the potential for appreciation and gains. All such investments are also subject to risks. The risks vary between different types of financial instruments and combinations thereof. Past performance should not be taken as an indication of future returns.

The analysis is not directed at U.S. Persons (as that term is defined in Regulation S under the United States Securities Act and interpreted in the United States Investment Companies Act of 1940), nor may it be disseminated to such persons. The analysis is not directed at natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign laws or regulations.

The analysis is a so-called Assignment Analysis for which the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published on an ongoing basis during the contract period and for the usually fixed fee.

Carlsquare may or may not have a financial interest with respect to the subject matter of this analysis. Carlsquare values the assurance of objectivity and independence and has established procedures for managing conflicts of interest for this purpose.

The analysts Markus Augustsson and Niklas Elmhammer do not own and may not own shares in the analysed company.

Similar News