Senior Equity Analyst

Equity research Zinzino: Preview Zinzino Q1 2026 – Some moderation of growth

16 Apr 2026

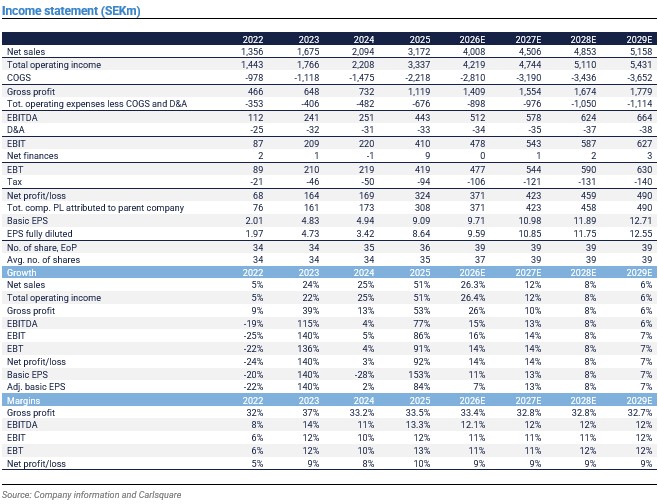

According to preliminary sales figures, total revenue grew by 26 per cent in Q1 2026, compared to 59 and 46 per cent in Q1 and Q4 2025, respectively. The growth slowdown is more significant than we had expected. The greatest negative deviation from our previous assumptions is in the North America and Eastern Europe regions. However, growth in the largest region, Central Europe, held up better than we had expected at +40 per cent (including acquisitions). Given the anticipated impact of acquisitions (~+28 per cent on sales), we infer that the group’s organic growth (adjusted for FX) was in the low single digits in Q1 2026.

Admittedly, the very solid growth in 2025 makes the comparison difficult. At the same time, new product launches should underpin sales. Adjusted for acquisitions, sales in North America appear to have contracted. However, we need to learn more about the contribution from acquisitions to gauge the underlying development.

We expect the margin to strengthen year-on-year also in Q1 2026 due to raw-material cost and FX tailwinds, further boosted by good operating leverage. We expect relatively weak cash flow, burdened by seasonal working capital fluctuations and acquisitions.

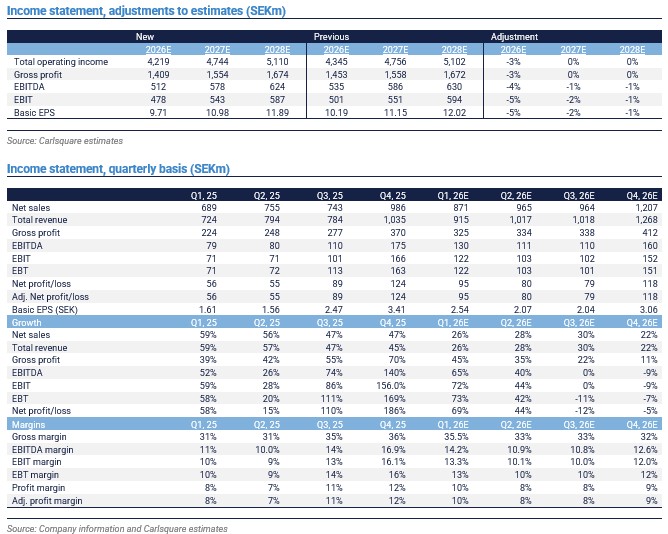

We have reduced our estimates somewhat, primarily due to a slower start to 2026 than previously expected (see table of adjustments below). We continue to anticipate variations in gross margins from quarter to quarter. Also, we acknowledge some uncertainty in our margin forecasts due to changes in the geographic mix, remuneration to distributors, and acquisitions that may impact outcomes.

Slight base case adjustment due to updated forecasts and relative valuation

We lower our base case valuation to SEK 215 per share (222) following adjusted estimates, but also lower peer group multiples (e.g., EV/EBIT NTM has depreciated to 11.4x from 12.5x). We estimate that the share trades roughly in line with other listed direct-selling companies (at an EV/EBIT NTM of 11.2x).

Read our latest research update here.

Disclaimer

Carlsquare AB, www.carlsquare.se, hereinafter referred to as Carlsquare, is engaged in corporate finance and equity research, publishing information on companies and including analyses. The information has been compiled from sources that Carlsquare deems reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be considered a recommendation or solicitation to invest in any financial instrument, option, or the like. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for either direct or indirect damages caused by decisions made on the basis of information contained in this analysis. Investments in financial instruments offer the potential for appreciation and gains. All such investments are also subject to risks. The risks vary between different types of financial instruments and combinations thereof. Past performance should not be taken as an indication of future returns.

The analysis is not directed at U.S. Persons (as that term is defined in Regulation S under the United States Securities Act and interpreted in the United States Investment Companies Act of 1940), nor may it be disseminated to such persons. The analysis is not directed at natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign laws or regulations.

The analysis is a so-called Assignment Analysis for which the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published on an ongoing basis during the contract period and for the usually fixed fee.

Carlsquare may or may not have a financial interest with respect to the subject matter of this analysis. Carlsquare values the assurance of objectivity and independence and has established procedures for managing conflicts of interest for this purpose.

The analysts Niklas Elmhammer and Markus Augustsson do not own and may not own shares in the analysed company.

Similar News