29 Jun 2026

Equity research Enrad, Q1 2026: A sluggish start, but the case remains intact

29 Apr 2026

Read the full research update here:

Enrad delivered negative growth in Q1 2026, which was distinctly below our expectations. The cost base was also slightly higher than anticipated. That said, inbound enquiries remain strong, and the company is not losing any tenders to competitors. As such, our long-term view on the case remains intact.

Weak start to 2026 in a still sluggish market

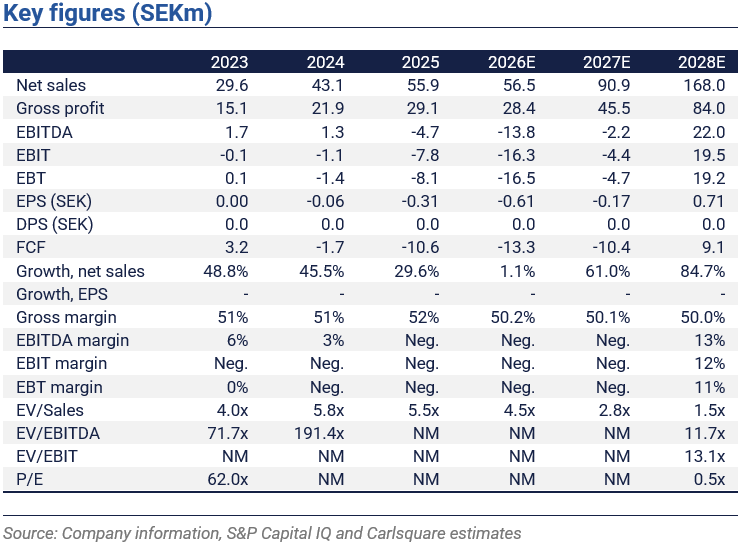

In Q1 2026, net sales came in at SEK 7.1m, down 56% YoY. This was also undoubtedly below our forecast of SEK 15.1m, implying negative growth of around 7%. Gross margin was 49.6%, broadly in line with what we see as a normalised level. A new initiative in Sweden weighed on OPEX, which totalled SEK 10.5m, and EBIT came in at SEK -7.0m (vs our forecast of SEK -0.5m). We estimate FCF in Q1 at SEK -9.9m, while cash at quarter-end stood at SEK 10.7m.

The long-term case is intact, but finances are pressured near term

Despite a weak start to 2026, the long-term investment case remains intact. The soft quarter reflects deferred demand rather than a structural drop-off. The company continues to report strong inbound enquiry flow across all key markets, with no indications of lost deals. The pickup in order intake at the start of Q2 supports management’s view that H2 2026 will be materially stronger, further underpinned by projects in the Netherlands and Belgium now moving towards decision phase.

Structurally, Enrad’s positioning is also unchanged. Manufacturing cooling and heat pumps based on natural refrigerants, with production in Sweden, is unusual. The regulatory and environmental tailwinds underpinning demand are, if anything, stronger today than when the case was first framed.

Near term, liquidity remains a risk. However, with a strong principal owner, which in our view has a long-term commitment and has previously provided support through various solutions, we see funding risk as limited. We are monitoring cash closely. A normalisation in order intake in Q2 is in our view a prerequisite for the company to execute its growth plan without additional capital.

Revised valuation

We have cut our net sales forecasts for 2026-28E by an average of around 17%, reflecting a sluggish market and limited visibility on when demand will accelerate. We have also raised the discount rate to reflect somewhat higher funding risk. In our base case, we derive a fair value of SEK 10.5 per share (SEK 11.5). Our fair value implies EV/Sales 2027P of 3.0x and EV/EBIT 2028P of 13.8x. The peer group is currently trading at a median EV/Sales NTM of 2.4x and EV/EBIT NTM of 17.5x.

Disclaimer

Carlsquare AB. www.carlsquare.se, hereafter referred to as Carlsquare, conducts operations in Corporate Finance and Equity Research and thereby publishes information about companies, including analyses. The information has been compiled from sources that Carlsquare considers reliable. However, Carlsquare cannot guarantee the accuracy of the information. Nothing written in the analysis should be regarded as a recommendation or invitation to invest in any financial instrument, option or similar. Opinions and conclusions expressed in the analysis are intended solely for the recipient.

The content may not be copied, reproduced, or distributed to any other person without the written consent of Carlsquare. Carlsquare shall not be liable for any direct or indirect damage caused by decisions made based on information contained in this analysis. Investments in financial instruments provide opportunities for capital appreciation and profits. All such investments are also associated with risks. The risks vary between different types of financial instruments and combinations thereof. Historical returns should not be considered as an indication of future returns.

The research is not directed at U.S. Persons (as that term is defined in Regulation S of the United States Securities Act and interpreted in the United States Investment Companies Act 1940) and may not be distributed to such persons. Nor is the analysis aimed at such natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign law or regulations.

The analysis is a so-called commissioned analysis where the analysed company has signed an agreement with Carlsquare for analysis coverage. The analyses are published continuously during the contract period and against customary fixed remuneration.

Carlsquare may or may not have a financial interest in the subject of this analysis. Carlsquare values ensuring objectivity and independence and has therefore established procedures for managing conflicts of interest.

The analysts do not and may not own shares in the analysed company.

Similar News